")

")

Yuriy Yakymenko, Razumkov Centre President

Vasyl Yurchyshyn, Razumkov Centre Economic and Social Programmes Director

For humanity, the early 2020s were marked with the growth of risks and challenges, which can slow down the generally positive dynamics of global development in previous years. This was not unexpected, since the period after the Global Financial Crisis of 2008-2009 brought signs of slowdown of global development, primarily due to the weakening of economic liberties — re-establishment of protectionist measures, cross-border barriers for the movement of goods, services, capital, people, which gave grounds to predict the emergence of a new global agenda: de-globalisation, increased isolation, and formation of new centres of political and economic gravity.

At the same time, under the influence of trade and technological confrontation between the two world-largest economies — the USA and China — new challenges of the world economic policy began to take shape, the response to which not always takes place within the framework of the existing global institutions, which can cause significant social and economic losses for these two economies and the world economy as a whole.

Along with this, Russia's full-scale war against Ukraine demonstrated how quickly a political crisis (especially that one that was previously considered unlikely) can lead to shocks in consumer and investment markets and result in market failure (even in stable developed countries). Such shocks have also demonstrated to the EU, US and other developed countries the interdependence between the general economic dynamics, access to resources, industry, trade and technologies, and the risk that arises when technology flows to unfriendly countries that have no scruples about economic and political abuses, which created the ideological prerequisites to "revise" the necessity and degree of observance and preservation of economic liberties — in the conditions of increased risks for the security of individual countries and even the global security system, which calls into question the appropriateness of preservation of the economic system that secured development over the past fifty years.

Macroeconomic and institutional shifts

The beginning of the 2020s was rich in global crisis processes. The coronavirus pandemic, not leaving the world economy a chance to recover, turned into another, almost "perfect storm" for the global politics and economy — the Russian invasion of Ukraine, which brought, among other things, crisis shocks for the world food and energy markets. Of course, in order to counteract shocks, countries (including large developed economies) have to balance internal needs and markets, which is usually difficult if the necessary mechanisms are not used properly.

This could not but affect the world economic system. First of all, it should be noted that the leading developed countries, which in the past five decades served as models of socio-economic development, visibly demonstrate poor economic dynamics. This is especially true for the EU that in the mid-2010s faced a series of internal (e.g., debt) and external (e.g., migration) crises, prompting the need to review the basic postulates of socio-economic development, on which European countries were built and developed after World War II.

At the same time, large emerging countries, primarily China and India, whose economic growth and development model were based on private entrepreneurship, but with active interference of state institutions in the economic processes, established themselves in the global politics and economy — with elements of the so-called controlled capitalism, where the government and business work together (but under the undisputed leadership of the state) towards a common goal. (In the case of China, such a goal is clear — to substitute the United States as the world economic leader, becoming global power No.1.) Different options of such a "national-centric" model were attractive for most emerging countries (many of which previously were viewed as subordinate periphery), for which authoritarian management of the economy was understandable and acceptable.

Therefore, China, India, Brazil and other emerging countries entered the global competitive environment, using their own versions of development based on entrepreneurship, inherent in the capitalist system of management, and the powerful "dirigism" inherent in autocratic states. In such conditions, the competitive confrontation increasingly turned into an "economic cold war", in which the dynamic emerging countries, with the active and even aggressive participation of national governments, won competitive advantages in the global distribution of production factors.

As a result, economists more and more discussed the need to review the development models in the leading developed (capitalist) countries. Let us note a number of features of the world development in recent decades, which largely reflect the mentioned controversial processes in the global economy.

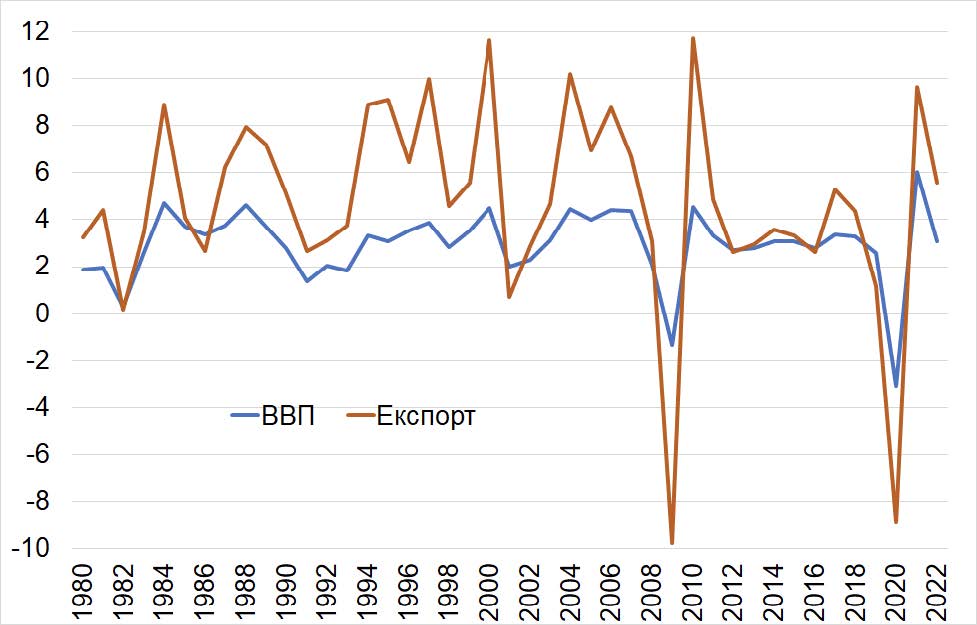

(1). First of all, it should be noted that in recent decades, which brought acceleration of globalization, international trade presented kind of an indicator and driver of economic soundness, and accession of emerging countries (including China) to international resource (mainly raw material) markets provided "cheap" supply of basic and intermediate products, which made it possible to sustain aggregate demand, thereby ensuring high economic dynamics and accelerated development of countries relying on the export-based development model (Chart "World economy and exports growth rates").

In recent years (after the Global Financial Crisis), the growth rates of the world GDP and world exports (trade in general) have almost equalled, i.e., the world trade largely lost its role in sustaining the overall economic dynamics (instead, the importance of internal factors has increased). Export-oriented (emerging) countries had to change the priorities of their national economic policy, and with that — to find new niches, primarily in foreign markets (trade, investments), along with state support for these sectors.

World economy and exports growth rates, % per annum

— GDP | — Exports

(2). Along with this, the deterioration of the global economic dynamics caused by crisis shocks also produced a feedback — it prompted countries to close their borders and concentrate on their problems, trying to secure themselves from external negative factors. Such attempts did not seem successful (in particular, pandemics know no borders, and the war in Europe affects almost everyone), but economic activity was limited, while the needs of foreign economic exchange brought about fragmentation (due to the intensification of contacts with "friendly" countries) of the world economy.

This caused a slowdown of economic growth in all parts of the world in recent years, further aggravated by intentions and actions aimed at separation from the world or isolation with a few partner countries. At the same time, the slowdown of economic growth means a decrease in incentives to develop economic contacts with the rest of the world.

This only emphasizes another controversial factor of the global development of the last decade. A number of "small" crisis waves (such as the migration and debt crises of the 2010s in Europe, although not global in scale, but quite sensitive even for developed countries) prompted those countries to increasingly build barriers not only to protect their own companies from global competitive pressure but also to escape being drawn into crises in partner countries. And it turned out that even the established global institutions (such as the World Bank, WTO), which were seen as capable to promote economic development, appeared incapable to solve the tasks of building economically fair global economic relations.

It also turned out that the competitive positions of many countries and companies, in the conditions of increased restrictions (on resources and logistics), are no longer as strong as it was believed. This was especially clearly manifested in industrial production, in particular, in Germany, whose industry during the past fifty years had competitive advantages thanks to the (politically motivated) preferential cost of Russian energy resources.

(3). It should also be noted that in industrialized countries, industry most often creates the main demand for transportation and logistics, promoting growth in other sectors and industries. However, in the last decade, the growth rates of the added value in the economy (GDP) and in industrial production have been almost equal (Chart "World economy and industrial production growth rates"), due to the mentioned "small crises" and the associated lack of stability needed for large-scale investment in industry, and the unstable political situation in many parts of the world. This was further aggravated by the gradual transition to the industry of the next generations, which requires a new resource base. And if at the beginning of the 2000s the main resources were associated with the extraction, distribution, and delivery of energy feedstock, which seemed stable and transparent, today, the situation is changing dramatically.

World economy and industrial production growth rates, % per annum

— GDP | — Industrial production

Further, Russia's invasion of Ukraine has shown that what matters the most is not the resources themselves and their current consumption but their forecasted strategic distribution, since they can be channelled to a competitive economy in order to, first, make them a "capital for the future" (in particular, with investments in green and digital technologies), second — to ensure resilience (and security) against potential geopolitical challenges, and third — to set priorities in the dilemma of the current efficiency and productivity of the economy compared to the strategic political and economic security.

In such conditions, despite the decrease of its share in the GDP structure, industry remains the centre of gravity and reflection of transformational processes and, accordingly, the industrial policy comes to the forefront, as a significant strategic and security component in the system of state governance. Governments around the world are introducing new regulations and launching new funding programs to support the domestic production of strategic products needed for sustainable growth — green and digital transformations, taking on new geopolitical and geoeconomic significance.

It should be noted that it was China that initiated strategic programmes aimed at the implementation of large-scale infrastructure projects to support the country's production and export capabilities. We speak about the Belt and Road Initiative, pushing the grand trade and investment infrastructure plan, which has demonstrated the inextricable link between industrial policy, infrastructure investments and trade expansion, and serves as a powerful tool of geopolitical influence in the recipient countries.

(4). It seems that security priorities in economic development gradually become dominant. Note that the share of consumption in the GDP structure of the largest economies shows tendencies to stabilize and even decrease (Chart "Consumption in the GDP structure"). In such conditions, greater savings mean a better ability to invest, and hence, the competitiveness of the economy, ensuring development and growth in the new geopolitical and geoeconomic conditions. Of course, export and investment expansion require security for the invested capital.

Consumption in the GDP structure, %

It should be admitted that governments increasingly interfere in resource allocation and industrial policies, and that such interference is intended to help national sectors achieve goals that markets alone are unlikely to achieve. This is not new and has always been practiced — using an industrial policy, governments sought to change the structure of economic activity to achieve certain corporate and social goals. In addition to the desire to introduce structural changes in the economy, an industrial policy was intended to rule out situations where market failures or lack of coordination among private actors prevent efficient allocation of economic resources.

Historically, the industrial policy often took the form of protectionism, introducing restrictions on certain supplies to strengthen import-substituting industrialization, i.e., it was mainly aimed at limiting or even banning imports, which, of course, significantly weakened the freedom of choice for economic agents. However, such intentions were not always properly implemented in practice. And in the second half of the last century, good governance was seen as the actions of government institutions that encouraged, rather than limited, economic freedom of business entities.

The coronavirus pandemic and the war in Ukraine demonstrated the intrinsic fragility of global supply chains (which "suddenly" stopped working) and the need to increase their resilience through processes such as friend-shoring and fragmentation, although this did not ensure access to the necessary components of production processes. Against the background of growing geoeconomic tensions, countries are increasingly concerned about the possible weakening of their strategic sectors or technologies, as well as the consequences for their economic growth, national security and innovative potential.

Friend-shoring and specific trade alliances, which began to multiply, provided some additional (favourable) opportunities of cross-border exchange for companies, but at the same time, they introduced additional risks, since now the owners and managers of corporations of a country have to take into account the interests (often politically determined) of corporations of other partner countries, with which the former may be unfamiliar, or which may conflict with their own interests and competitive needs in different sectors.

Note that nowadays, non-fiscal and tariff tools for the protection of national markets, as short-term response to (un)expected challenges, are becoming increasingly important. Globalization challenges and interdependence of even remote economies require state management tools at another — institutional — level, including with account of coordination even between friendly economies.

For interaction and coordination (as far as possible), the leading countries form an institutional field in two (conventional) domains. The internal one is formed by legislative and regulatory acts specifying the features of the new economy, including export bans (e.g., on advanced semiconductors and equipment for their production). In this way, in the USA, the Inflation Reduction Act (IRA), the Critical Raw Materials Act and the Net Zero Industry Act have become fundamental laws that determine the features and tools of countering current and future threats to economic development (primarily concerning green and digital transformation) of the leading developed countries.

The external domain is associated with the emergence, as we mentioned, of new industrial and trade unions of partner countries, the purpose of which is mutual encouragement of advanced technologies, while barring them to unfriendly countries (especially if there is a threat of their use for aggressive purposes). A typical example is the Chip 4 Alliance (USA, Japan, Taiwan and Korea), or the G7 Partnership for Global Infrastructure Investments, commenced in 2022, including under the influence of political and military processes caused by Russian aggression.

Such institutional domains of state governance become especially relevant in the context of implementation of the goals and needs of green and digital transformation, which require significant (new) resources, both for the abandonment of traditional sources of economic growth and the formation of new future-oriented production, logistics and technological networks.

Resource dependencies

As the world prepares for major industrial and technological changes required for the digital and green transformation, the mismatch between supply and demand for production factors, which determine the current competitiveness of national industries and the prospects for maintaining the appropriate level of competitiveness, is becoming increasingly apparent.

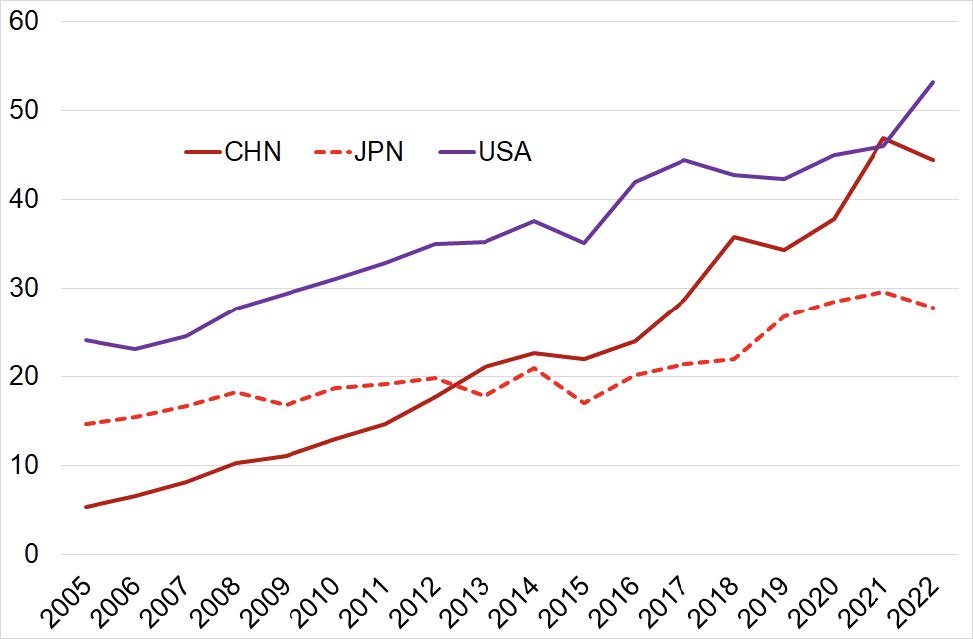

Let us note two aspects. The first one is intellectual, describing to what extent a country is involved in the production and use of intellectual products (national and international). First of all, we should note that the USA is the leader in the official use of intellectual property (Chart "Royalties"). Meanwhile, China, which in the 2010s followed the path of Japan at the beginning of the "Japanese miracle" in the 1950s—1970s, actively purchasing foreign intellectual products, has caught up with the USA in the expenditures on intellectual property (significantly overtaking Japan, which for a long time was second in such expenditures) (Chart "Royalties...paid"). That is, there are reasons to claim that Chinese scientists and engineers have access to most of the technological innovations of the day. Moreover, given the criticism of the Chinese government for its disregard of the fight against the illegal use of foreign intellectual property, the access of Chinese companies to advanced technologies is likely to be even wider.

Royalties, $ billion

paid

received

At the same time, China is ever more actively entering the intellectual property markets, thanks to the achievements of its scientists and specialists. While in 2015, the country’s revenues for the use of its intellectual property made less than 1% of such revenues in the USA, in 2022 this figure exceeded 10% (Chart "Royalties...received").

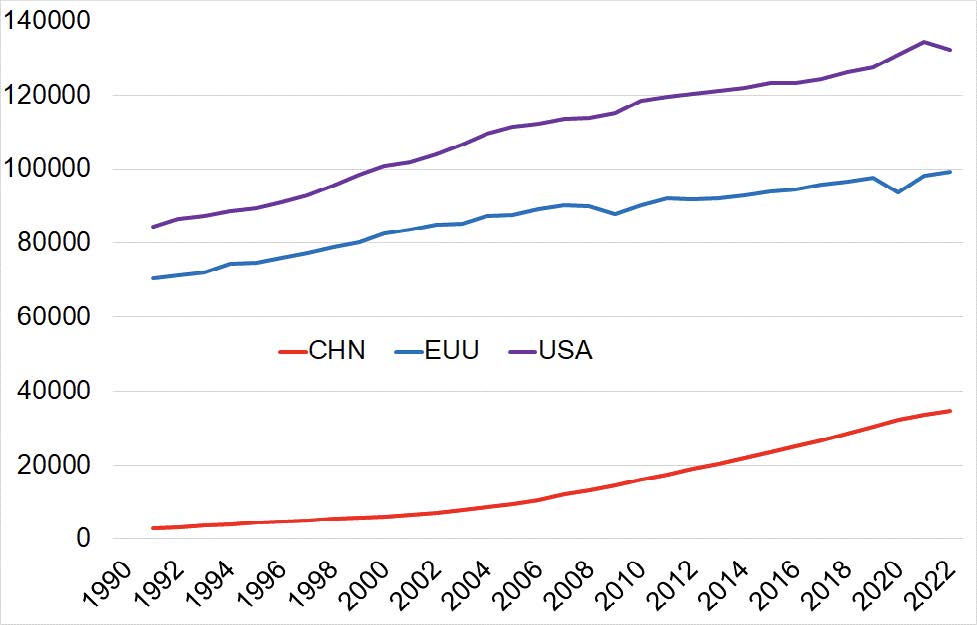

There are reasons to claim that this (systematically promoted) approach allowed China to significantly advance in two directions. First, to significantly raise labour productivity (added value per employee) in the national economy (GDP per employee Chart).

GDP per employee, $, purchasing power parity, in 2017 prices

While in the mid-2000s, the productivity in the USA exceeded that of China 10–12 times (in the EU — 9–10 times), at the beginning of 2020, this excess decreased to 4 and 3 times, respectively. In addition to the economic impact, this also has a significant social effect: accelerated formation of the middle class in China, whose demand will become an additional factor in the growth of volumes and productivity of the economy.

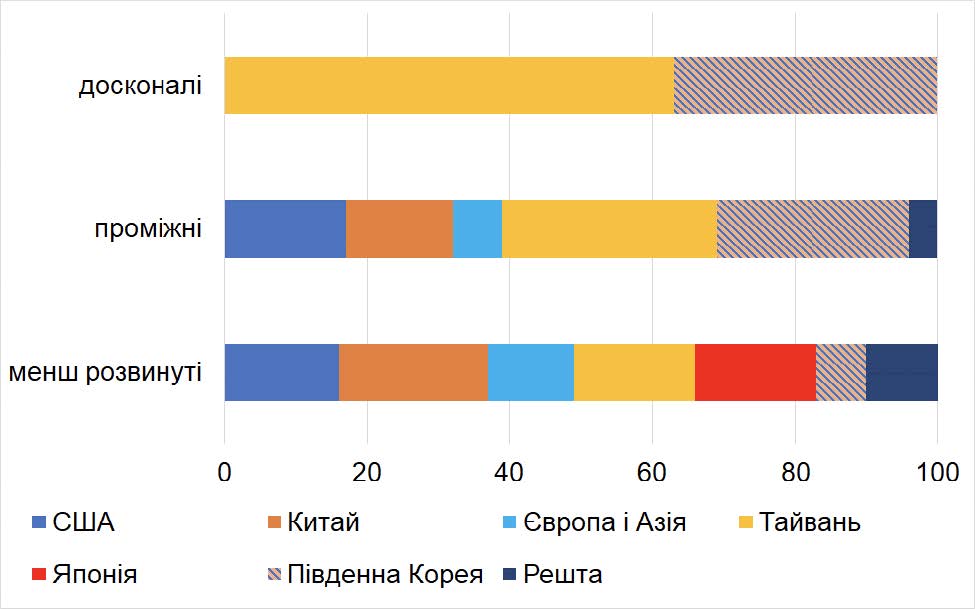

Second, China's active conquest of previously inaccessible production niches, set to guarantee the country's economic success today and in the near future. First of all, it is about chip production. A decade ago, the USA, the EU, and Japan were considered the absolute leaders. Today, production is highly concentrated in a few Asian countries. At the same time, production volumes and complexity (including capacity and size) in Western countries are noticeably "slumping". The most advanced chips (less than 10 νm in size) are produced only in Taiwan (63%) and South Korea (37%) (Chart "World chip production").

World chip production, %

perfec | intermediate | less advanced

USA | China | Europe | Asia Taiwan

Japan | South Korea | Rest of the world

Now, let us focus on the second aspect: raw materials, being a component of technological modernisation (whose importance will surely increase). Surprisingly, issues related with access to raw materials have come to the forefront in recent years. In particular, there is an increase in demand for the key commodities, including the so-called "critical minerals". So far, the access to them has not become a bottleneck for increasing productivity and advanced technologies. However, difficulties in access and supply may well be expected there in the near future.

One important reason is that today China possesses a significant part of mineral and raw resources (including rare earths metals) critical for the current technological revolution, primarily, green and digital transformation. Moreover, China not only owns most of the world's resources but it is also the first to take steps (including within the framework of the Belt and Road Initiative) aimed at strategic investments in Africa and South America, to get access to critical raw resources on this basis. We are not sure that China will be willing to share its strategic reserves with its opponents.

This appears more than relevant, considering that first the pandemic, then the war in Ukraine and the growing concern about rapid climate change made governments to intensify the energy transition and to decarbonize national economies by implementing the so-called carbon neutrality, which, in turn, leads to the increase of state financial support and the development of new environment-friendly technologies.

However, the green and digital transformations require coordinated regulation, for which the proper institutional framework has not been created yet (the WTO is unable to cope even with "traditional" trade disputes, and for new problems it simply does not have the necessary authority and trust).

Therefore, there is a big question about the future of the green technologies and China's role as the world's main supplier of basic components. At the same time, there is a global controversy regarding the security of commodity supply chains. First of all, it concerns China's claim to a dominant position in the supply chains of critical minerals, not only in their extraction but also in processing, which already has an economic basis, as China has made large investments in critical minerals and products of their processing not only domestically but also, as we mentioned, in the emerging foreign countries.

Mineral-rich emerging countries, in their turn, seek to enhance the competitiveness of their mining sectors and raise investment. These countries pursue policies capitalizing on their mining and processing industries, although they also strongly depend on the country's infrastructural facilities, since the processing facilities are energy intensive. Therefore, China's investments in infrastructure sectors in Africa, South America and Asia within the framework of the Silk Road Initiative fully meet the needs of both sides. Of course, in such conditions, China will receive undisputed strategic benefits, irrespective of competitiveness.

Meanwhile, the developed countries, particularly those poor in critical minerals, are investing in disruptive technologies that can influence the demand, introducing substitutes and optimizing production and consumption structures, which can significantly hinder green transformations. However, although at the initial stages this may lead to an increase in production costs, the strategies of risk reduction developed by the EU and the US may, in the long run, reduce the dependence of Western countries on imports from China and other emerging countries, controlled by China.

Such an approach can undermine market efficiency and lead to the growth of decarbonization costs, making it difficult to achieve global carbon neutrality goals. In addition, in order to achieve its ambitious goal of carbon neutrality by 2060, China itself (if it really pursues the stated goal) may have to reduce its role as the world's main supplier in order to meet its obligations. So, despite the similar goals of raising competitiveness, the initial positions of the leading political and economic actors do not look compatible (if they are not confrontational).

Along with this, there are a number of global processes that still inspire optimistic expectations. Indeed, in recent years, the USA and the EU have placed an unprecedented emphasis on economic security, the policy of reducing strategic dependencies and state funding aimed to secure technological advantages in the areas that will shape the future.

On the way to strategic capitalism

Of course, developed democracies are especially concerned about attempts to master advanced technologies and their possible use for military purposes. The USA and EU are consistently introducing legislative and institutional mechanisms to control the access of third countries to advanced technologies created in partner countries (box "Limitations on entering the club of supercomputers").

LIMITATIONS ON ENTERING THE CLUB OF SUPERCOMPUTERS

On October 7, 2022, the US implemented export control mechanisms to hinder China's ability to source, develop, manufacture or even purchase advanced semiconductor technologies. Its main goal is to prevent China from gaining access to the most advanced chips. In connection with the new policy, US and foreign companies that use US technologies must stop supplying technological innovations to China's leading technology corporations.

Such measures and steps are intended to slow down China's progress in advanced quantum and supercomputers and the possibility of practical development and military use of artificial intelligence (AI).

Traditionally, the USA used to be the undisputed leader in supercomputers and the AI sector. However, over the past 10 years, the US advantage over China shrank dramatically, partly due to China's rapid growth of investment in science and technology research, as well as difficulties in the US in the production of the most advanced computer microcircuits.

At the same time, competition (including in the supercomputer industry) prompts the US (through the Chip and Science Act) to step up expenditures on research and development, microchip production, and to introduce export and investment restrictions in the field of chip development and production

In fact, this legislative and institutional regimentation of security priorities in the economy meant that the US and the EU are moving from (traditional) market capitalism to a new form of strategic capitalism, through decisive state interference in strategic and security-sensitive sectors of economy. A renewed industrial policy becomes central to strategic capitalism.

Noteworthy, states have traditionally applied the industrial policy to correct market failures, i.e. situations in which market mechanisms cannot be relied upon for rational and efficient distribution of public costs or benefits. Under strategic capitalism, the industrial policy is aimed at the development of internal economic capabilities and stability in strategic sectors of the economy for protection against the attempts of rival states to seize highly competitive niches in the world economy and the global distribution of resources.

The ideology of strategic capitalism helps understand current transformations in the economic policy, where states increasingly interfere in the management of foreign economic flows, development and spread of technologies. Meanwhile, the relations between the state and business in different sectors differ significantly. In sectors that are considered strategic, states try to regulate and coordinate business transactions and exchanges, while other sectors (their majority) continue to operate on market principles. We note that instead of allowing market forces to function freely within the framework of international economic relations, states increasingly take active steps when their strategic (primarily, security) interests are at stake.

In the current decade, Western countries have suffered from numerous external shocks, such as the coronavirus crisis and the war in Ukraine (in which democratic countries allied with Ukraine), and faced new challenges, including related to digital and energy transformations. This led to a dramatic change in economic strategies, which incorporated targeted measures with numerous tools of interference in industrial and trade issues. Moreover, the dependence on foreign entities in the supply of critical goods and resources intensified efforts aimed at removing such economic imbalances, which could not but cause an increase in political confrontation.

We note that the demand for and need of protective and control measures will only grow, because today the risks of "trade wars" are a reality, and such "wars" can well turn armed confrontations (as witnessed by the situation around Taiwan). This should take place simultaneously with the countries searching the lines of economic policy (including economic incentives for development), choosing the right paths among a number of alternatives and introducing appropriate measures for proper macroeconomic balancing and acceleration of integration processes.

Since 2020, three global shocks sharpened criticism of the market capitalism’s ability to dominate global development. First, the coronavirus pandemic resulted in an alarming shortage of production capacities (even for essential goods) in Western economies. Second, the Russian aggression led to unprecedented economic sanctions, but they turned out not as effective as they were intended to be. Third, the dire consequences of global climate change became apparent, their remedy requires significant volumes of critical raw materials in the absence of appropriate capacities, even in the medium run.

This led to an increased perception of control and coordination management as a new reality, where interference of the government in various spheres of the economic system is criticised, as before, the difference being that strategic capitalism is driven by goals and objectives in which the state focuses on control of strategic assets.

The world economy is gradually drifting towards strategic capitalism. In contrast to the free-market capitalism that has prevailed in recent decades, by resorting to geoeconomic measures, governments set the conditions under which transactions in goods, services and technologies can be carried out, and where foreign business partners are deemed reliable. Companies are trying to preserve their businesses as much as possible, but at the same time recognize that they have limited control over the unfolding geoeconomic shifts.

Strategic capitalism does not rule out state interference in economic processes. Instead, it shows how security considerations become a common factor of such interference. However, it turns out that the concept of security can have many manifestations and go beyond those associated with the so-called strategic branches of the economy.

The dynamics between geoeconomic measures taken by governments and corporate governance will determine how much the world economy will deviate from the current market system (with its economic liberties) and to what extent it will be subordinated to the national strategic choice.

Science-intensive enhancement of competitiveness

Supporters of liberal markets are sorry to admit it, but there is an impression that the state interference in economic decision-making and economic processes will grow. To a large extent, this is due to the increasing difficulty for large leading countries to remain highly competitive (in the world economy), while the emerging (primarily Asian and Pacific) countries, with the direct participation of their governments, actively implement transformations in access to and use of technological achievements.

If we look at the changes in the Global Competitiveness Index, we can see that the ratings of the leading countries (except the USA) over the past year (the assessment is based mainly on the data of the previous year) have experienced negative pressure (Table "Rankings in the Competitiveness Index"). Even China after abandoning its "zero covid" policy failed to restore its competitiveness, as dynamic emerging countries quickly occupied the vacant niches. Of course, competitive losses, especially of European countries, are to a large extent caused by Russian aggression and sanctions. However, in the new trade and energy realities European countries will need to implement green and digital transformations.

Rankings in the Competitiveness Index

|

|

2019 |

2020 |

2021 |

2022 |

2023 |

|

USA |

3 |

10 |

10 |

10 |

9 |

|

China |

14 |

20 |

16 |

17 |

21 |

|

Germany |

17 |

17 |

15 |

15 |

22 |

|

France |

31 |

32 |

29 |

28 |

33 |

|

Taiwan |

16 |

11 |

8 |

7 |

6 |

As Europe's competitiveness lags behind the other parts of the world, the EU should focus on raising public and private investment in technology and skills and actively promote green energy transformation for reliable supply of clean energy.

Certain "inhibiting" changes are also taking place in the field of digital competitiveness (table "Rankings in the Digital Competitiveness Index"). Interestingly, even China failed to improve its position in the digital environment, although this area has been and remains closely monitored by the Chinese leadership. Perhaps the reason is that China is unable to reach Taiwan's level of chip production, which hampers further technological applications.

Rankings in the Digital Competitiveness Index

|

|

2019 |

2020 |

2021 |

2022 |

2023 |

|

USA |

1 |

1 |

1 |

2 |

1 |

|

China |

22 |

18 |

15 |

17 |

19 |

|

Germany |

17 |

18 |

18 |

19 |

23 |

|

France |

24 |

24 |

24 |

22 |

27 |

|

Taiwan |

13 |

11 |

8 |

11 |

9 |

With the energy component, the situation is different. According to the Energy Transition Index, firstly, the ratings of the USA and China are lower than those of the leading European countries. Secondly, China still lags behind the leading developed countries both in terms of actual implementation and readiness for such transition (table "Rankings in the Energy Transition Index"). And although it declares the goal of meeting its obligations of decarbonization, it at the same time uses the opportunity, sharply increasing purchases of Russian oil and gas after the imposition of sanctions on the aggressor by democratic countries.

Rankings in the Energy Transition Index, 2023

|

|

Total score |

System efficiency |

Readiness for transition |

|

1. Sweden |

78.5 |

81.0 |

74.8 |

|

7. France |

70.6 |

73.3 |

66.5 |

|

11. Germany |

67.5 |

64.6 |

71.9 |

|

12. USA |

66.3 |

68.4 |

63.2 |

|

17. China |

64.9 |

65.0 |

64.8 |

It seems that this gap will rapidly be closed, as China leads both in terms of physical infrastructure and investments in renewable energy sources (as components of this rating). However, it is not ruled out that the slowdown of the leading countries is temporary, due by the need to solve urgent security issues, since, along with the mentioned expansion of the intellectual sphere (creation and use of intellectual property), countries have been increasing the scientific capacity of their economies over the past decade, in particular, by boosting investments in research and development, as well as in industry.

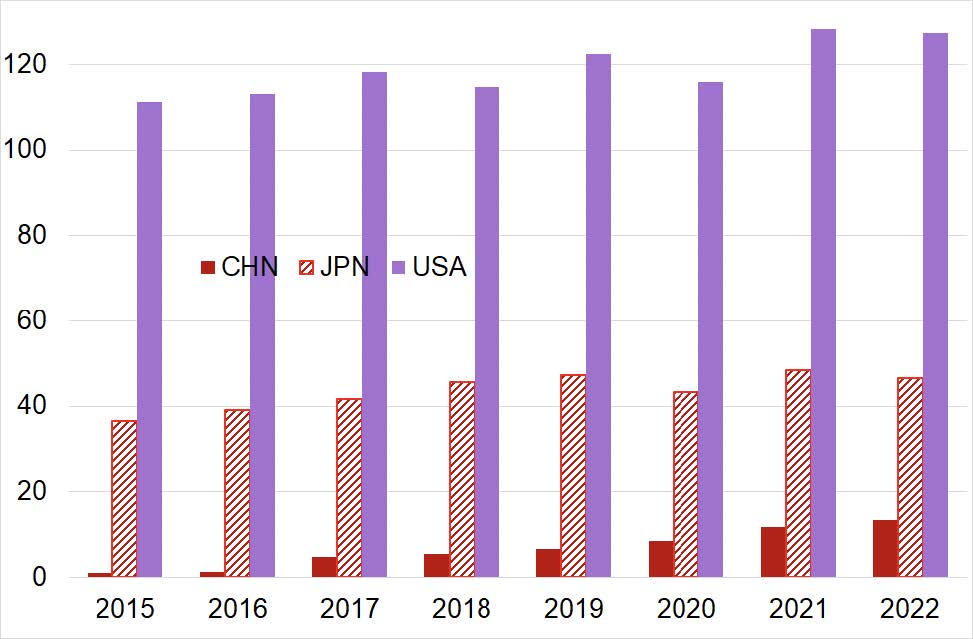

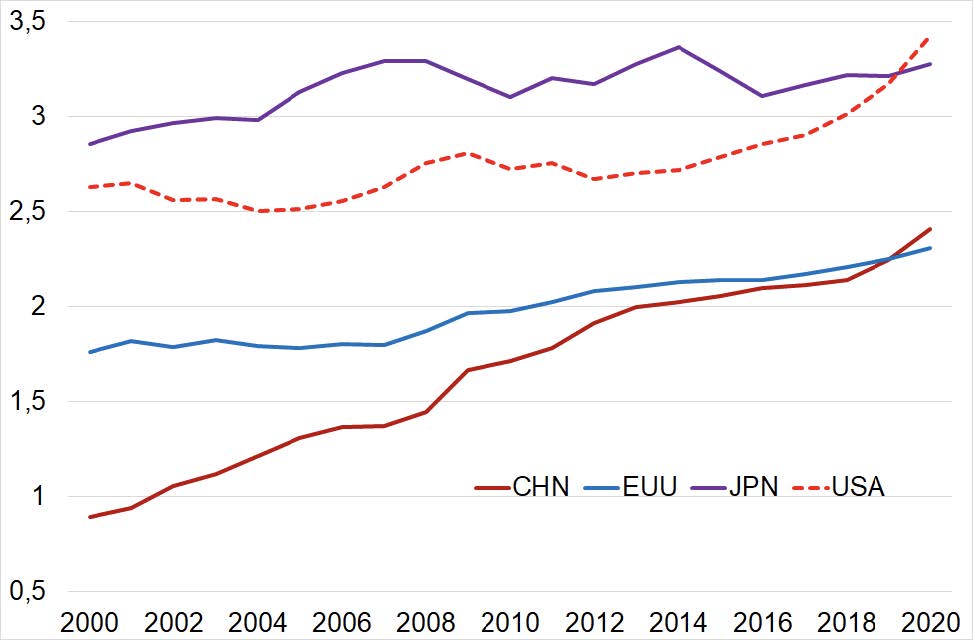

In recent years, China has overtaken the European Union in terms of funding (as a share of GDP) of scientific research and development (R&D) (chart "Expenditures on research..."). And although it lags behind Japan in this respect, taking into account the size of the Chinese economy, in absolute terms, the expenditures on research in China, as well as the size of its economy in general, are gradually approaching those of the US and are already far ahead of Japan.

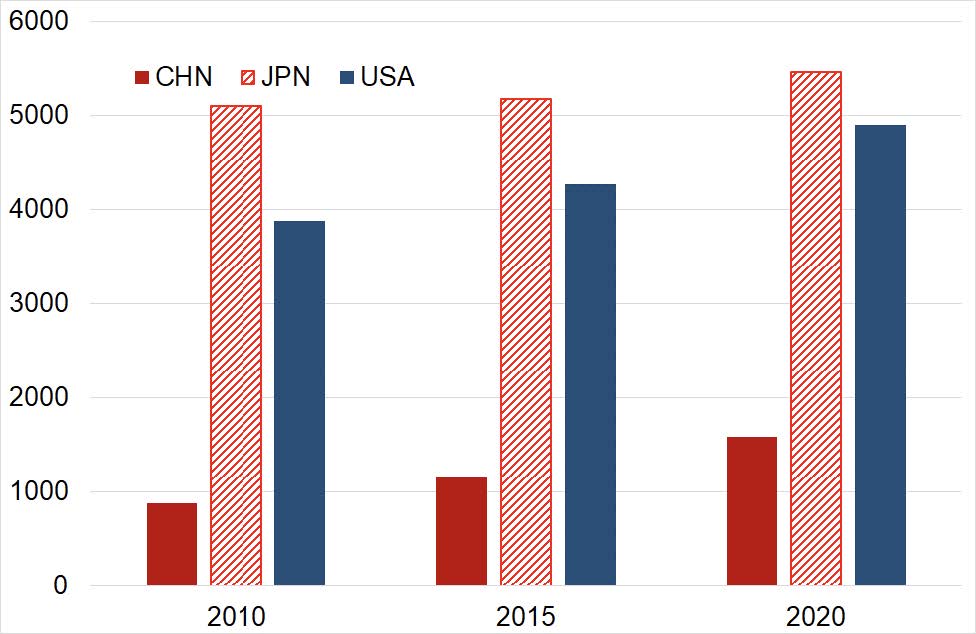

A similar closure of the "gap" between China and the USA and Japan (with their recognized scientific and research schools) is also observed in the number of scientists. Lagging behind in relative terms (the number of scientists relative to the country's population), China now has far more scientists than Japan, and will soon catch up with the United States (Chart "Scientists per 1,000,000...").

Expenditures on research and development, % of GDP

Scientists per 1,000,000 residents

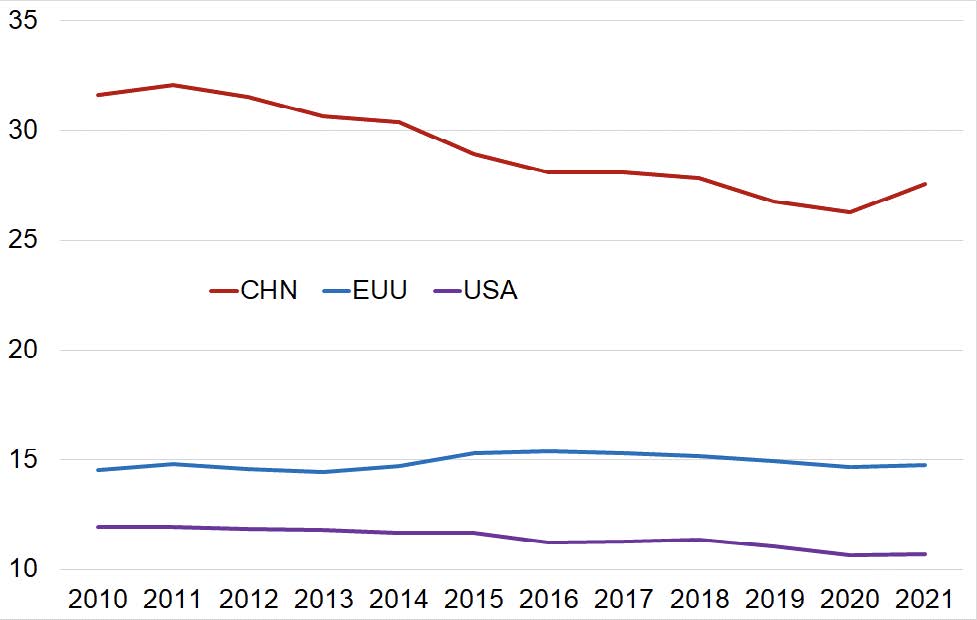

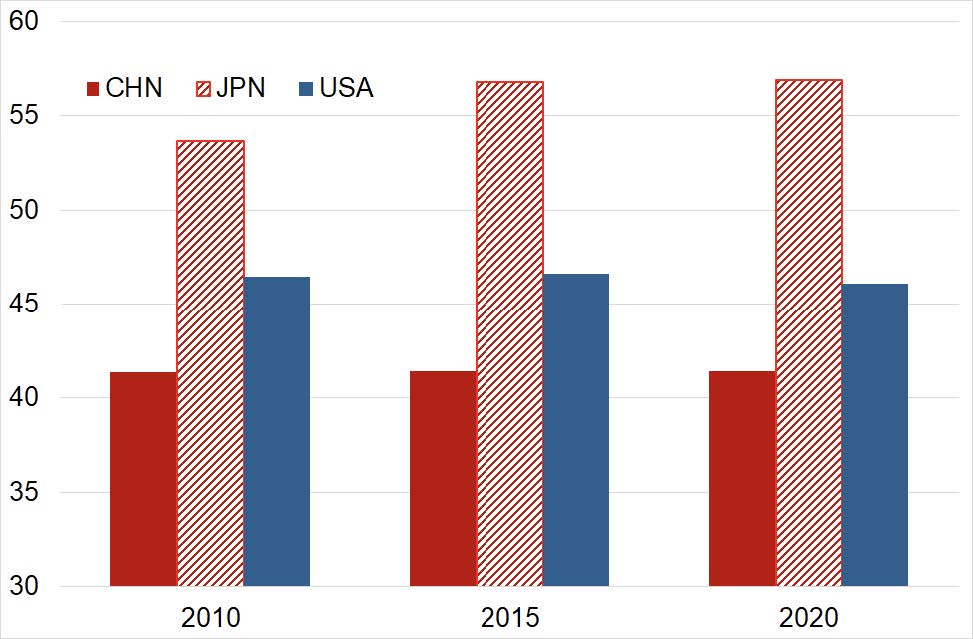

Along with this, high absolute indicators (of production, scientists, technicians) do not yet determine technological progress, especially in industry. Say, in China, about a third of the added value of the economy as a whole is created in the processing industries, while in the leading developed countries this share makes 10–15% (chart "Share of processing industries..."). However, the share of technological production in China has practically not changed over the past decade (40–42% of the processing sector), which is significantly lower than in the USA (55–57%) (Chart "Medium- and high-tech industries"). This confirms the popular opinion that the quality of many goods produced by Chinese companies is still inferior to American and European technological goods.

Share of processing industries in the economy, % of GDP

Medium- and high-tech industries, % in total processing sector

Therefore, the leading countries — primarily the USA and China — are trying to accelerate the science- and technology-intensity of their economies, which will become an important component of transformational (green and digital) processes and secure high competitive positions. Along with this, the leading countries of the world began formulation of a new economic policy, a characteristic feature of which is the green and digital transition, as well as strengthening the security component in the strategic foundations of modernised state governance systems.

Place of Ukraine

Today, Ukraine, which is still fighting the Russian aggressor, is at the crossroads of two "perfect storms". On the one hand, acceleration of transformations (green and digital) in the world economy, which, in turn, significantly accelerates the technological renewal of the world economic environment. On the other hand, the country should resolutely and promptly introduce bold and ambitious processes of recovery, with the aim of forming a new economic and security environment, to become a natural element of the European economic space.

Ukraine cannot interfere in the economic struggle of the leading countries, such as the USA and China. However, it can consistently prove by its example that orientation towards the leading American and European countries, their economic values, institutions and markets create exceptional opportunities for soonest recovery, including thanks to extensive secure partner support.

The post-war reconstruction of Ukraine will take place under new territorial, financial, material, and humanitarian conditions. Even when the entire territory of the country is liberated, a significant part of its land will be unfit for economic activity for at least a decade (due to ruinations and mining). The loss of traditional raw materials, on which the domestic economy was built (coal, metals), as a result of their looting and destruction, means that the country needs to form the foundations for life in accordance with the challenges of green and digital transformations. The tasks will be complicated by the decrease in the number of the country's residents and the working population after the war, compared to the pre-war period, including as a result of the outflow and displacement of huge masses of the population.

In such conditions, even if in the future it is possible to maintain the aid from the USA, the EU and other countries at the level of 2022–2023, restoration of the production, transport, and humanitarian infrastructure, taking into account their scale, will lag behind the needs of the country that becomes a full member of the European community. Meanwhile, restoration of the infrastructure and reconstruction of the economy will create a steady demand for investment goods, which is possible only under conditions of soonest integration.

Therefore, the model of economic recovery of the country should be straightforward and transparent, to be supported by the business and population, restricting government interference, to that and governments can focus on constructive recovery (in line with the ideology of strategic capitalism). First of all, it is about (finally) supporting small and medium businesses, as the most adaptive, effective and efficient component of the domestic economic space. Pre-war governments worked in the paradigm of restrictions and withdrawal (by fiscal and administrative measures) of financial resources from successful economic agents. Preservation of the country's economy during the period of coronavirus and Russian aggression to a large extent became possible thanks to the reduction of unproductive governmental pressures. Therefore, it is inappropriate for the government to restore "traditional" methods of state management of economic processes, it should rather look for ways to liberalise business.

Along with this, cultivation of "new champions" — enterprises and companies (state-owned and private) that will embody the new face of Ukraine can offer a large space for government assistance, in particular, in the development and manufacture of defence equipment and weapons based on digital technological solutions, as well as assumption of a leading role in hydrogen energy, which will become the basis of provision of resources for a free and independent country.

In addition, the government will have to take care of the purity of the capital entering the country. Regardless of the need for resources, under no circumstances should the capital and investments of companies from unfriendly countries be allowed into the country's economy. And, of course, no contacts with Russia, as well as with those who continue cooperation with the aggressor.

https://razumkov.org.ua/statti/ideologichni-osoblyvosti-onovlennia-ekonomichnykh-svobod