")

")

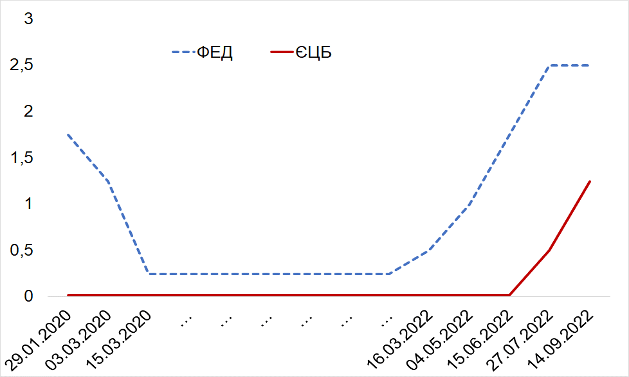

The European Central Bank (ECB) decided to sharply raise base interest rates (from September 14, 2022, by 75 basis points (bps)) — to 1.25%, for the second time in the last two months (previously — on July 27, by 50 bps). The main factor behind this increase is high inflation (its average rate in 2022 is expected to reach 8.1%), as well as the need to reduce the lag of the interest rates of the Euro zone behind the US rates (diagram "Base interest rates").

Base interest rates of the US Federal Reserve (FED) and the European Central Bank (ECB)%

International experts are convinced that the ECB will have to continue the policy of raising rates, as current inflation and projected inflation next year (5.5%) far exceed the target level of 2% (ECB’s main duty).

Meanwhile, further emphasis on price stabilisation in the Euro zone may be complicated by the need to promote economic growth, i.e. the ECB will have to decide on its priority — to curb inflation (with increased risks of economic slowdown, and therefore, possible unemployment growth), or to prevent recession due to expensive energy resources. Curbing inflation by raising interest rates may not be efficient enough, since the rise in consumer and, especially, producer prices is largely related to the (politicised) cost of imported energy resources (which the ECB cannot influence).

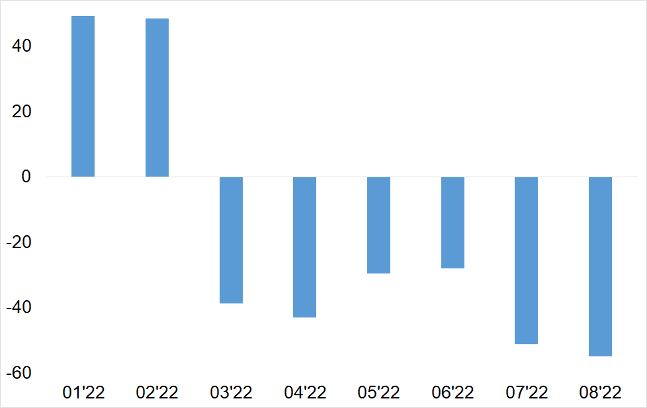

It must be admitted that today, the risks of the European economy falling into depression cannot be ignored. In particular, one of the leading indicators of doing business shows a clear downward trend (chart "Economic sentiment index"[1]) — the economic sentiment index in the euro zone fell to -54.9 in August, being the lowest since November 2011. This drop is definitely connected with the energy crisis in Europe. Since it is not known how quickly the crisis will be resolved, the duration of negative expectations remains uncertain.

Economic Sentiment Index

Attention should be paid to one more aspect of the need for the ECB interest rate to "not break away" from the key global financial indicators — the rates of the US Federal Reserve (FED). Base rates in the leading countries determine both the market rates (including at money markets) and the profitability of government securities (primarily, long-term bonds, debentures).

The dollar strengthening in recent months, as indicated, was caused, among other factors, by the active US interest rate policy (the chart "Base interest rates" above). Since significant volumes of capital flows are sensitive to the level (difference) of profitability (interest rates), the exchange rate dynamics of even the strongest currencies noticeably reacts to interest rate changes. Therefore, it is quite fair that the ECB (in addition to the anti-inflationary effect) raised rates to prevent the outflow of capital from Europe to the US, and thereby to support the euro[2].

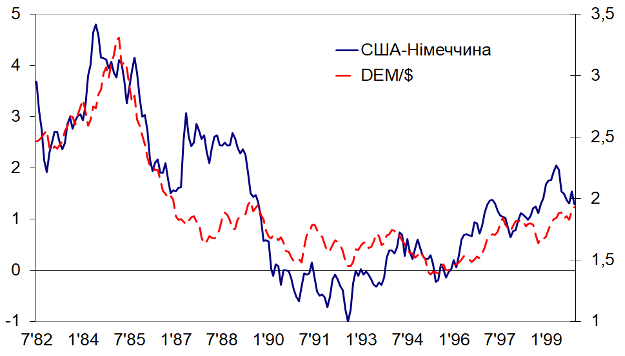

Yield difference between the US and Germany (pp, left scale) and the German mark (DEM) to the US dollar exchange rate (right scale)

Mutual dependence of the exchange rate dynamics of the leading world currencies and the difference in the yield of long-term government bonds is well illustrated by the comparison of the respective dynamics of the US and Germany in 1980-1990 (diagram "Yield difference between the US and Germany and the German mark to the US dollar exchange rate"), when the leading currencies were actually "freely" floating, which did not rule out some agreements of a principled nature[3].

What does the increase in the ECB base rates mean for Ukraine? In the short term, it is likely to remain imperceptible. The fact is that Ukraine operates in a special financial "regime". Extensive financial assistance is provided by countries and international institutions under special conditions, due to the Russian aggression. Grants (mainly, in USD) or loans of minimum value (not related to capital markets) account for a significant part of the aid.

Much more important for Ukraine today is whether the European Union will show solidarity (as it does to support Ukraine, countering Russian aggression), and whether it will withstand the risks of a cold winter (in case of energy limitations). If the economic needs of the Europeans (maintenance of usual well-being) prevail over the principles and values (human rights to life and freedom) on which the democratic world is built, then Ukraine will see negative consequences — weakening of the unity and cohesion of the EU countries with Ukraine, a decrease in political and financial aid for defence and post-war reconstruction of the country, weakening of humanitarian support for Ukrainian society.

[1] It describes the sentiments of institutional investors in Germany. Positive values of the index indicate optimistic sentiments regarding business development, negative values indicate pessimistic sentiments. Larger values correlate with higher optimistic or pessimistic sentiments.

[2] It seems that a cheap euro might support economic growth in the euro area due to more favourable conditions for European exports. However, for Europeans, it may bring a significant increase in oil and gas prices, quoted in dollars. That is, cumulative benefits may be not seen.

[3] The Plaza Agreement stands out among all known currency agreements. In the early 1980s, the rapid strengthening of the US dollar (as a result of the Reaganomics policy) relative to other currencies of developed countries aggravated macroeconomic imbalances. The tools of balancing were supposed to include a decrease in the value of the dollar and, accordingly, strengthening of other currencies, which was to balance exports and imports, and hence, capital flows among the largest economies. The measures applied (although not all the agreements were implemented) together with extensive mutual interventions led to the desired dynamics of exchange rates — over the next two years the dollar lost approximately half of its value (chart "Yield difference between the US and Germany and the German mark to the US dollar exchange rate").

https://razumkov.org.ua/komentari/yevropeiskyi-tsentralnyi-bank-sliduie-za-federalnym-rezervom-ssha