")

")

Today, there is little data about the current state and nearest prospects of the domestic economy: official information about the performance of individual industries and the economy in general is practically absent. In such conditions, the demand for comprehensive studies of the public and expert opinion is significantly growing, and polls (of course, always somewhat biased) remain almost the only source of information about the socio-economic situation in the country.

In Ukraine, the results of surveys among company heads and top managers about the performance and expectations of their enterprises are presented regularly (usually, quarterly, which is sufficient under "normal" conditions). However, such surveys rest on different methods, cover different enterprises or groups of enterprises, which significantly complicates generalisation[1]. It is not surprising that estimates may differ substantially[2].

In this context, the information released by the State Statistics Service of Ukraine "Expectations of industrial enterprises regarding the prospects of development of their business activity by types of economic activity and main industrial groups (2022)" seems interesting. It rests on monthly surveys of three-month prospects, that is, produces floating three-month estimates. Despite the importance of this presentation, it should be noted that the study only provides estimates of expectations but contains no information on the extent to which such expectations were met.

Let us look at some important indicators regarding the expected changes in the production volume / the number of employees in the branch in general.

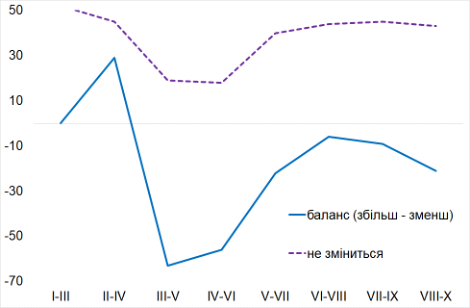

If at the beginning of the year, expectations of positive and negative changes in industrial production were almost balanced (more than 50% of respondents did not expect changes, and the number of positive and negative assessments differed little), in spring, negative expectations significantly prevailed (table "Expected changes in industrial production volumes...").

In the summer months, expectations improved significantly. In fact, almost half of the enterprises were convinced that there would be no significant changes in industrial production in the next three months. However, the question remains open, whether the situation will worsen (a decrease in production volumes), because enterprises have already "reached the bottom" in their production activities and "it will not get worse" (pessimistic interpretation), or (optimistic interpretation) stabilisation of the economic situation is finally taking place, and positive changes are possible in the future.

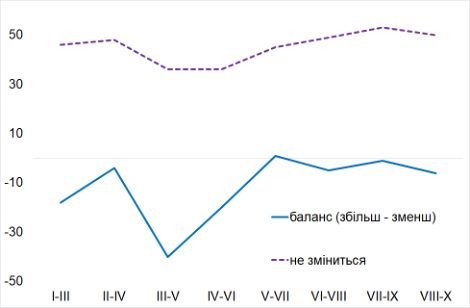

The situation is somewhat different with the assessment of expected changes in the number of employees (table "Expected changes in the number of industrial employees in the next 3 months"). Now, more than 70% of respondents is convinced that there will be no changes in the number of employees, but at the same time, the difference between those who expect a decrease and those who expect an increase in employment is significantly larger, compared to the production volume expectations.

Expected changes in industrial production volumes in the next 3 months

|

|

I–III |

II–IV |

III–V |

IV–VI |

V–VII |

VI–VIII |

VII–IX |

VIII–X |

|

Balance (up–down) |

-4 |

7 |

-41 |

-34 |

-18 |

-12 |

-10 |

-9 |

|

Will not change |

52 |

51 |

33 |

34 |

42 |

46 |

48 |

47 |

Expected changes in the number of industrial employees in the next 3 months

|

|

I–III |

II–IV |

III–V |

IV–VI |

V–VII |

VI–VIII |

VII–IX |

VIII–X |

|

Balance (up–down) |

-3 |

-1 |

-31 |

-30 |

-22 |

-20 |

-17 |

-15 |

|

Will not change |

81 |

79 |

61 |

59 |

66 |

70 |

71 |

71 |

Strong expectations of absence of changes in the number of employees even during the aggression may witness that a significant number of enterprises tried to retain their employees (especially qualified ones), and the employees themselves did not hurry to leave, considering the significant decrease in vacancies. Therefore, the expected decrease in the number of employees in autumn is not necessarily bad — it may indicate that employees feel freer in the search for new vacancies and are ready to look for a better job.

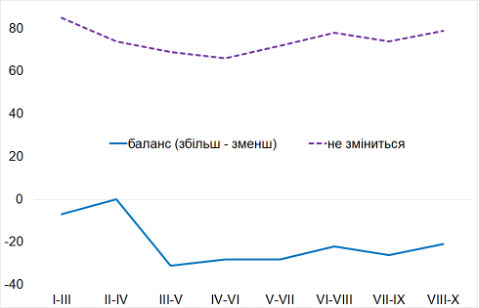

Of course, the general situation varies significantly, dependent on the industry. Let us look at metallurgy and the food industry.

Expected changes in production volumes in the next 3 months

| Metallurgy | Food industry |

|

|

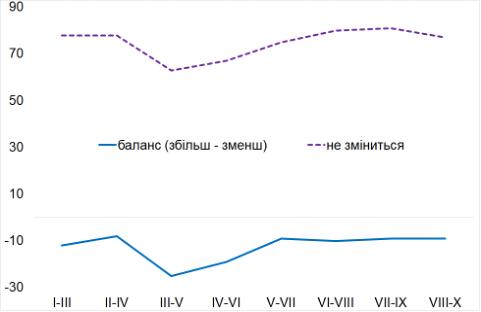

Expected changes in the number of employees in the next 3 months

| Metallurgy | Food industry |

|

|

With the beginning of the Russian aggression, expectations in metallurgy worsened significantly, while in the food industry — not too much (and in the short term). This is understandable, since, firstly, metallurgy suffered direct significant losses and ruination, and secondly, there is a stable domestic demand in the food industry (40-50% of respondents were convinced in the absence of changes) (diagrams "Expected changes in production volumes in the next 3 months")

Differences are even more evident in estimates of the number of employees (diagrams "Expected changes in the number of employees in the next 3 months"). In metallurgy, the opinion of a further decline in employment (by approximately 30 percentage points) is firmly held. In the food sector, more than 80% of respondents is sure that the number of employees will not change significantly, which may be seen as a sign of stabilisation in the work of the industry enterprises.

In other industries, the situation is different, but ever more answers point to equalisation of expectations of changes for the better and for the worse, with an increase in the number of neutral expectations. This may be seen as a sign (although not unconditional) of a trend towards stabilisation not only in expectations themselves but also in real production indicators.

[1] See, e.g.: Business predicts a decline in the number of employees at its enterprises. — https://speka.media/viina/ (NBU survey in the II quarter of 2022).

Production expectations of business are improving, but the assessment of the economic situation and state policy has worsened. — https://interfax.com.ua/news/economic/ (poll of the Institute of Economic Research and Policy Consulting (IER), July 4–14, 2022).

[2] The NBU study in the II quarter says that the domestic business "...expects a decline in the volume of production of goods and services as a result of a full-scale war and is pessimistic about the business activity of its enterprises", as well as "...a decline in the number of employees at its enterprises".

The IER notes that the domestic business "... thanks to the improvement of production expectations, plans to increase production and employment in the next three months."