")

")

Households always tend to save money, especially at a time of war and great losses. Today, it should be admitted that the national banking system successfully introduces tools that provide some protection for the monetary resources of households from sharp depreciation.

This is especially important for current and short-term purchasing power and maintenance of a "normal" wellbeing, since households themselves have extremely limited access to bank resources — bank loans to households in February-October decreased by 11% (from UAH 268 billion to UAH 238 billion ). Of course, banks see the high risks of resumption and growth of lending to households, and the situation is unlikely to change fundamentally in the near future. That is, households should rely on their own savings in future expenses.

Along with this, visible changes are observed in household deposits. We have already indicated a rapid increase in their volume (mainly thanks to timely and full payments to the military) — in February-October, total household deposits rose from UAH 774 billion to UAH 964 billion (+27%) (Household deposits chart). Let us note some structural features related to the need to preserve public funds, at least partially preventing their depreciation.

Household deposits

█ household deposits, UAH billion

— share of deposits in the national currency, % of total

So far, such tools are not enough. Given the current risks associated with a possible protraction of the war, the most reliable way to secure savings in hryvnias is to buy cash foreign currency. Of course, in times of trouble, households try to "stockpile" cash dollars, bearing recognised value for all potential economic agents under any conditions.

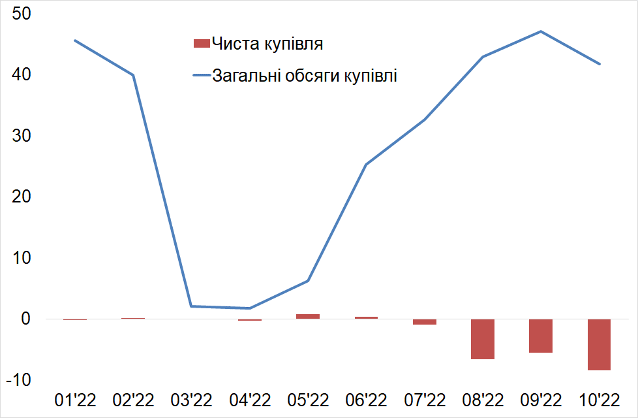

However, the associated benefits for the population have a "reverse" side for the monetary system — devaluation pressure on the exchange rate, which will require currency interventions, and with them, loss of the country's currency reserves. Therefore, from the very first days of the aggression, the NBU rightfully introduced a ban on free purchase of cash currency. As a result, purchases and sales in the cash markets fell record low, and the balance became zero (only the volumes bought previously were sold). Meanwhile, financial stabilisation in the summer of 2022 renewed the ability to buy and sell, and of course banks sold more currency than the population did (resplenishing the "stockpiles" of cash dollars) (diagram "Purchase of cash currency by the banking system from the population").

Purchase of cash currency by the banking system from the population, UAH billion

Net purchase

Total purchase

Understanding the attractiveness of dollar savings for the public, the NBU introduced a number of so-called currency liberalisation measures, expanding access to non-cash currency resources ("hedging" devaluation risks). For example, back in July, the NBU, simultaneously with the official devaluation of the hryvnia (refusal to maintain the UAH29.25/$1 rate), allowed natural persons to buy non-cash currency from banks with subsequent placement on term deposits for a period of at least 3 months, which in a certain way can be considered as a means "relieving" the pressure on the cash currency markets.

In line with the same "ideology", the NBU introduced six-month "swaps" (purchase of currency for six-month deposits with reverse sale at the NBU exchange rate). Given the fact that the NBU is trying to contain sharp exchange rate fluctuations, such "swaps" have a stabilising effect on hryvnia savings of households (although only owners of large deposits can get a real profit). At the same time, real dollars do not leave the banking system.

Although these instruments did not gain strong popularity, they nevertheless influenced the structure of household deposits: the hryvnia value of deposits denominated directly in foreign currency increased (their share in national currency decreased — see the Household deposits diagram), including due to the gradual devaluation of the hryvnia. At the same time, part of household funds is tied up and cannot immediately enter the cash markets, which has a (minor) anti-inflationary effect

Today, there are reasons to believe that the larger part of Ukraine’s territory will be liberated from the invaders, and more households will need funds for reconstruction. Therefore, it is extremely important that until the days of liberation, the population's losses of savings are minimised.

Thus, the NBU needs to continue the search for tools (perhaps somewhat specific, given the peculiarities of the country's current financial environment), probably with a link to dollar assets (which are trusted by the population). Other areas of effective use of savings lie in the sphere of privatisation, corporatisation, shareholding, which can quickly become the basis for the recovery of stock markets, and therefore — stabilisation and economic growth.

https://razumkov.org.ua/komentari/pro-resursy-domogospodarstv-ii