")

")

Of course, the Russian visit of the Chinese leader was mainly connected with the possible expansion of military support for the aggressor. However, there are reasons to claim that the economic factor played a no less important role in the development of political and diplomatic processes.

The Joint Statement of the two leaders on deepening comprehensive strategic partnership to jointly shape a new era, on the one hand, confirmed the ambitions of both countries in uniting the Global South to counter the Collective West. On the other hand, it showed China's concern in creating a wider circle (around BRICS or the SCO) of "partners" for successive displacement of liberal-democratic principles from the foundations of the new era (as seen by autocratic states). China's economic success and economic strength are of great importance for the attainment of these two strategic goals.

The past three years were not very successful for the country. At the end of last year, China parted with its "zero COVID" policy and badly needs new economic achievements. Now, the country faces economic challenges caused by the Russian aggression and the risk of sanctions, which will be much more painful than the benefits of cheap trade with Russia.

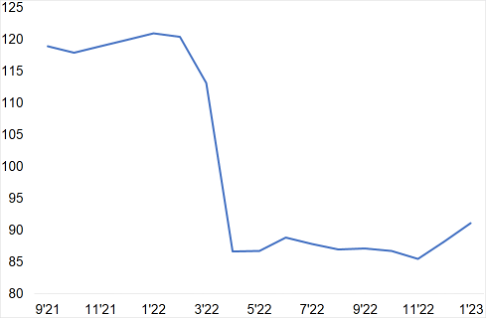

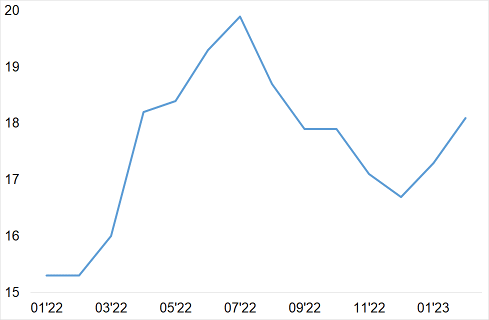

Internal economic problems. The planned economy growth by 5% does not seem easily achievable, in particular, due to the low level of consumption (set to make the basis for the transition from the export-oriented model of the Chinese economy to domestic consumption). Moreover, consumer sentiment does not want to improve and is significantly lower than in the pre-coronavirus period (Consumer Sentiment Index chart; hereinafter, unless indicated otherwise, the quoted data are to be found here. At the same time, significant concern of the authorities is caused by high unemployment among the young people, which after the shock growth in the spring of 2022 does not show a steady decrease and remains at a level of 18% (Youth Unemployment chart), which is unacceptable for Communist China.

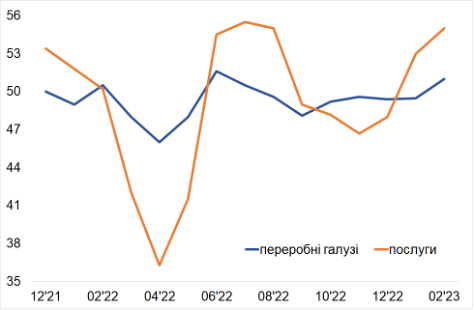

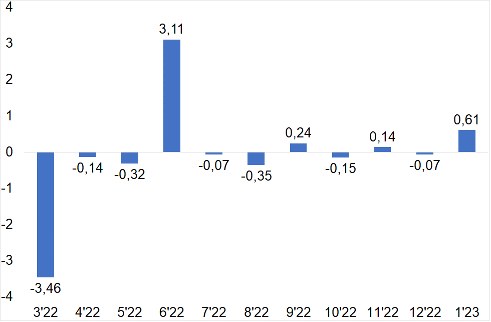

The current economic dynamics do not promise a fast recovery of industry (Business activity chart). Noteworthy, the dynamics of production (processing industry and services) are quite weak and unstable (which is especially noticeable in the service sector) and show no signs of acceleration (Business activity in China's processing industries and services sector chart). Likewise, the dynamics of retail sales remain weak (which confirms the uncertainty of households in the end of crisis periods) (Retail sales dynamics), while car sales (one of the most important indicators of household well-being) fell to their lowest level in a year (Car Sales chart).

Therefore, in the conditions of insufficient domestic consumption and weak global demand (as a result of the continuing crisis manifestations in many countries of the world), one may hardly expect a significant growth of the Chinese industry, which could become the basis of the expansion of world production, as was the case in the previous decades.

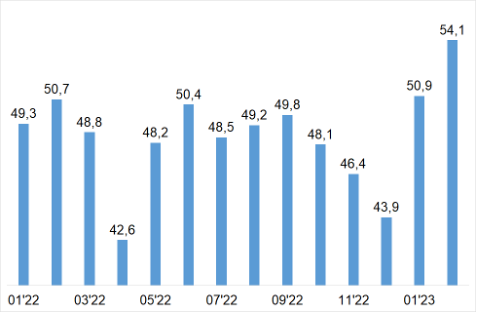

And while indicators of new orders have improved since the year beginning (New Orders Index chart), they still remain low for accelerated economic recovery. Therefore, if we still expect acceleration in the country's economy, it concerns the service sector. First of all, tourism, travel, hotels, which were actually closed in the previous three years due to the "zero" coronavirus policy. However, their opening may whip up domestic prices and increase inflationary risks.

Therefore, China's economic dynamics are unlikely to return to pre-coronavirus levels in the coming years. The obstacles will include high interest rates, negative demographic factors, restoration of state control over leading corporations (including private). Moreover, we should expect stricter control of the financial system, hi-tech and innovation sector.

Consumer sentiment index

Youth unemployment, % (according to polls)

Business activity in China's manufacturing and service industries, indices

processing industries services

Index of new orders

Retail sales, % of growth compared to the previous month

Car sales, millions

It should be noted that the current economic processes in China are in a marked contrast to expectations after China's decisive step taken in the fall of 2022, when the country opened its borders to foreigners for the first time in three years of the pandemic, as it gave up the policy of zero tolerance to COVID. However, the fear of repeated lockdowns has a negative impact on consumer sentiment and expectations, and thus, as indicated, significantly limits restoration of sustainable economic dynamics attractive for emerging countries.

So, China urgently needs to solve its internal problems, not laying them off for a long time. The tacit consent to a greater Chinese presence in the Russian southern regions of Siberia and the Far East may contribute to migration of the population to such "new" regions, and therefore, to the labour supply, which will reduce unemployment, especially among young people, and improve consumer expectations of households.

Foreign economic ambitions. For the Chinese leader, the visit to Moscow was probably even more important internationally. Although the attention to the visit largely focused on "what Russia got", for China, it was another step towards the formation of a "new world", where Chinese influence will spread and grow.

The point is that China (and Russia) do not hide their dissatisfaction with the domination of the dollar in world finances. Over the past decade, they have been repeatedly calling for the de-dollarization of world finances. At the same time, it is already clear that de-dollarization will be accompanied with yuanization.

In this part, there is even an "achievement" in terms of involving "third" countries. As a result of the sanctions policy, the main consumer of Russian oil and gas — the EU — cut Russian imports. The excess supply, which led to a sharp decrease in the price of those resources, was absorbed by China. However, this does not solve the issue of the long-term energy demand of China's growing economy (given the risks of falling under the secondary sanctions of developed countries). Therefore, China is strengthening cooperation, primarily in the energy sector, with the Gulf countries now. In terms of imports, these are long-term contracts for the supply of crude oil and liquefied gas. In terms of export and hi-tech cooperation — growth of investments in production, storage and transportation of oil and gas.

To promote cooperation, China promotes the introduction of new and fast financial (so far, settlement) instruments minimizing the dollar "intermediation". Therefore, we are actually talking about the emergence of the concept of petroyuans — internationally acceptable instruments (to support extremely vast financial arrays in bilateral relations so far), which will be based not on the dollar but on the Chinese currency — the yuan. That is, dollarization is to be replaced with yuanization, at least partially.

Moreover, economic agents of other countries may also drift toward yuanization. For example, a number of financial institutions in India are introducing a payment channel that will use Chinese yuan for trade between India and Russia.

As for Russia itself, during the visit, Russia declared its readiness to expand not only mutual payments in yuans but also to use yuans in trade settlements with emerging economies of the Global South (Asia, Africa and South America). Of course, such concession could not but please the Chinese leader, as it is a direct step to strengthening China's position in countries that are already suffering from problems with "cheap" Chinese loans taken earlier.

Hence, Russian support for yuanization of world finances strongly helps China's global leadership ambitions.

However, this is not the end of China's interests. Since China will consistently push de-dollarization, yuanization will require a change in the structure of the country's reserves. Today, the lion's share of China's (and Russia's) reserves is kept in dollars (long-term government bonds).

For Russia, the change in the structure will be solved simply — the share of yuans will grow (in particular, as a result of the growth of exports of energy resources and raw materials to China). For China, it seems appropriate to increase the share of gold in its reserves, which can serve as a basis for expanding and strengthening the new payment system in the process of international yuanization.

Noteworthy, at the beginning of 2023 Russia ranked 5th in the world in terms of gold reserves (2,299 tons), China — 6th (2,011 tons) (table "Gold and currency reserves". However, China's demand for gold may grow (indirect confirmation is that at the end of 2022 the volume amounted to 1,948 tons and has been maintained at this level since November 2019), including due to a decrease in the dollar share.

Gold and currency reserves

|

|

Gold reserves |

Foreign currency reserves |

|

China |

2011 tons |

$3133,2 billion |

|

Russia |

2299 tons |

$574,2 billion |

Hence, it may be assumed that at the meeting, the parties discussed the sale of part of Russia's gold reserves to China, of course for yuans, which perfectly fits into the paradigm of yuanization. Of course, such issues can be resolved only at the level of the highest leadership of the country.

How it can affect Ukraine. It may be stated that Ukraine has clearly and definitively decided on its strategic priorities, key partners, the values that help the country withstand the military pressure of the Russian aggressor.

Therefore, in addition to a clear idea of the prospects of socio-economic and socio-political reforms, Ukraine must take into account the geopolitical and geoeconomic interests of strategic partner countries in the conditions of global polarization, that is, to be extremely careful with economic proposals coming from countries not seen as allies by our main partners — the USA, Great Britain, Canada, the EU and others.

In the domestic political community there may again be those who will call for the restoration of economic contacts with China, which is allegedly making political and diplomatic efforts to end the war. However, Ukraine should not succumb to the phantom of quick benefits from growth of trade or yuanization. First of all China should decide on the level of its support for Ukraine and correlation of its interests in Ukraine with the interests of the current strategic partners.

Ukraine courageously continues to fight against the aggressor. So, freedom and independence must be strengthened on the economic front as well.

https://razumkov.org.ua/komentari/ekonomichni-skladovi-vizytu