")

")

Recently, we addressed the issue of inflation at the global and national level, as well as the role of central bank rates in countering inflation. High inflation in the leading developed economies, including the USA and the EU, in the summer of 2022 forced the central banks to abandon the policy of low (zero) interest rates, which was practiced during the coronavirus period, and to introduce strict monetary measures.

One of the most efficient anti-inflationary tools is presented by high base rates set by central banks. At the same time, the central banks of big economies are guided by the policy of the US Federal Reserve (FED), which largely determines the trends in the global financial system. The current FED measures against global inflationary shocks are expectedly triggering changes in the policies of central banks of other countries.

Inflation crisis. Today, both the inflation rate and inflation expectations in the leading (and emerging) countries are close to record-high in recent decades (table "Annual inflation in 2020–2022"), so, the leading banks, following the USA, are pursuing or will introduce a policy of long-term rate increases. This will give significant macroeconomic effects: weaken growth incentives for the real sector of the economy, on the one hand, and affect the value of the national currency, foreign trade and investments, and debts, on the other.

Annual inflation in 2020–2022, %

|

2020 |

2021 |

2022* |

|

|

USA |

1.2 |

4.7 |

8.3 |

|

Great Britain |

1.0 |

2.5 |

9.9 |

|

Germany |

0.5 |

3.1 |

7.9 |

|

Japan |

-0.02 |

-0.23 |

3.0 |

|

China |

2.4 |

1.0 |

2.5 |

|

Turkey |

12.3 |

19.6 |

80.2 |

* — as of September 2022 (year to year)

In the leading countries, annual inflation in 2022 is close 10%, only China and Japan managed to keep inflation within the "desired" range of 2±1%. The low inflation rate in China is largely attributed to the new wave of the pandemic with its restrictions, as well as to the crisis in the real estate market. For Japan, which has experienced deflation for years, 3% is a high inflation rate.

Due to the high inflation, most countries slowed down economic growth or even show a decline. In the 2nd quarter of 2022, compared to the previous year, a drop of 0.6% was recorded in the USA, 0.1% in Great Britain, and 2.6% in China. There were some "paradoxical" exceptions — surprisingly, hyperinflation in Turkey (over 80%) did not prevent the country from showing the growth of 7.6%.

Another anti-inflationary step by the FED. Governments view inflation as the main source of trouble for the national economies. To counteract it, the US FED on September 21 again raised the base rate by 75 basis points, to 3-3.25% — the highest level in the last 15 years (since the global financial crisis of 2008). Announcing the increase in interest rates, the FED emphasised that this decision was taken to reduce the aggregate demand, prevent overheating of the economy and avoid long-term imbalances.

The Bank of England also raised the base rate by 50 bps, to 2.25%, being the highest indicator since 2008. A week earlier the European Central Bank (ECB) raised its interest rate by 75 bps, to 1.25%. Only the Bank of Japan maintained a negative interest rate policy (-0.1%).

Although anti-inflation measures have been pursued since 2022, they were seen as a legacy of the coronavirus and household support programmes. However, the Russian aggression against Ukraine significantly expanded the problem to include the disruption of global energy and agricultural markets, which brought significant imbalances in those markets, and price shocks in consumer markets in general.

By raising base rates, central banks do not expect a quick reduction in consumption. Such an increase is to lower the demand in "expensive markets" — of cars, real estate, etc. Although it means weakening of economic activity, in the current conditions (inflation of almost 10%) it is deemed acceptable.

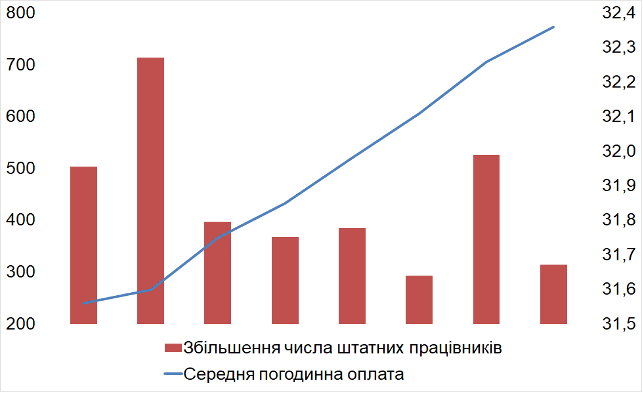

Implementation of a stricter policy by the FED was not a surprise, they were preparing for it. Wages continued to grow, as did the employment, albeit at a slower pace (diagram "Average hourly wages...").

Average hourly wages (seasonally adjusted, $/hour, left scale)

and increase in the number of full-time employees (thousands) in the private sector

— Increase in the number of full-time employees; — Average hourly wages

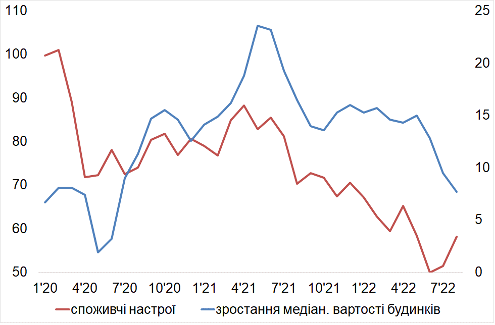

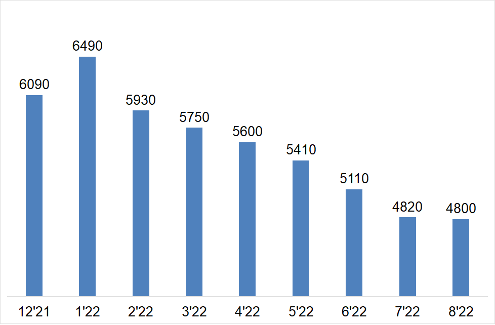

The willingness to invest has decreased, as a reflection of the uncertainty of households in maintaining their purchasing power (diagram "Index of consumer sentiment..."). Thus, although the increase in the value of houses has slowed down sharply, the willingness to buy a house has also decreased (diagram "Sales of existing houses") due to risks related with the ability to service loans in the near future (keeping in mind the losses of the US real estate market caused by the crisis of 2007–2008).

|

Index of consumer sentiment (left scale) and growth in the median value of houses (%, compared to the corresponding period of the previous year) |

Sales of existing buildings, thousand |

|

|

|

— consumer sentiment; — growth in median house value |

Since strong anti-inflation measures hinder economic growth, it is important to understand when the rate hikes will stop. The rates may well continue to rise in the first quarter of 2023. However, the unemployment rate may be one of the criteria for changing the FED policy. Now, unemployment in the US is kept at 3.6%. By 2023, unemployment is expected to reach 4.4%. Upon reaching this level, the policy of curbing inflation (by increasing the interest rate) may change to a policy of growth and encouragement of economic activity.

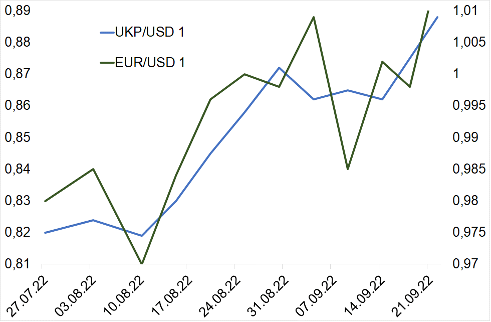

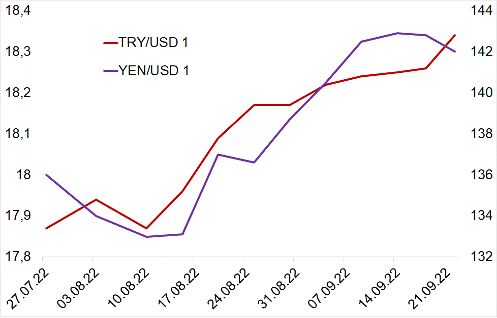

Contrary influences. US interest rate hikes often generate strengthening of the dollar against most currencies. Since the previous rate rise in July 2022, the dollar has noticeably appreciated (chart "Currency exchange rates to the dollar").

Currency exchange rates to the dollar

|

British pound (left scale) and euro (right scale) |

Turkish lira (left scale) and Japanese yen (right scale) |

|

|

However, this year saw a certain peculiarity of the influence of the exchange rate dynamics on other macroeconomic indicators. Since the softening of the US monetary policy in March, there have been fears that the expensive dollar may stir up imports and shrink exports, causing losses in the US trade balance.

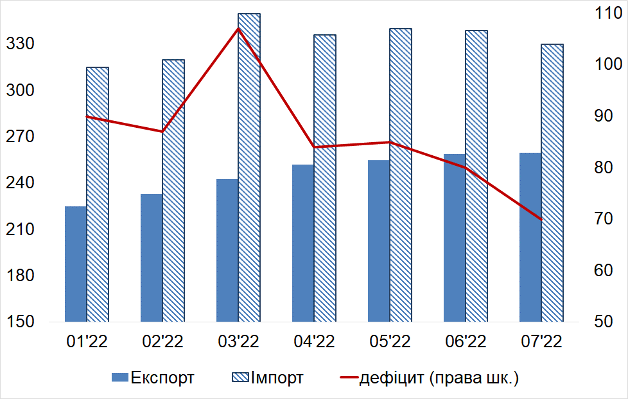

Now, the situation is just the contrary — there is a noticeable increase in exports while imports are stable, with a relevant decrease in the foreign trade deficit (diagram "Foreign trade in goods and services"). So far, there is no breakdown by country and industry. However, it may be assumed that the US boosted energy exports to help the EU overcome the energy supply deficit caused by the Russian aggression.

Foreign trade in goods and services, $ billion

Exports; Imports; Deficit (right scale)

To sum up — Ukrainian implications. As we noted in our previous reviews, the increase in the dollar value against other currencies will not have a significant impact on Ukraine in terms of access to resources or the cost of new borrowings. It is extremely difficult for a country fighting for independence to hope for favours from the world financial markets, that is, market credit resources are actually barred for Ukraine. Today, the sources of funds only include aid, grants and soft loans (mostly in dollars) from international financial institutions and leading developed countries.

The weakening of the euro (and other currencies) relative to the dollar, to which the hryvnia is bound, may affect the balance of payments. However, Ukraine's exports to the EU are dominated by agricultural products, which are listed in dollars, so, they little depend on the UAH/EUR exchange rate dynamics.

The exchange rate can slightly impact the revaluation of the reserves. However, the share of euros in the NBU gross reserves is low (about 6%, equivalent to $1.4 billion out of the total $25.4 billion), and their impact will also be low. Assets denominated in British pounds or Japanese yen are even smaller — approximately $0.35 billion each.

Ukraine may also suffer from the weakening currencies of its key trading partners: it may lead to the loss of competitiveness of domestic producers. However, Ukraine has proactively implemented anti-crisis measures (much tougher than its partners) prompted by the Russian aggression. It raised the base interest rate to 25% and devaluated the national currency from UAH 29.25/$1 to UAH 36.57/$1, effectively creating a "safety margin" to reduce the impact of devaluation of other currencies. The import of inflation (increase in consumer prices abroad is transformed into hryvnia prices of imported goods) will take place in Ukraine, but its scale will be insignificant.

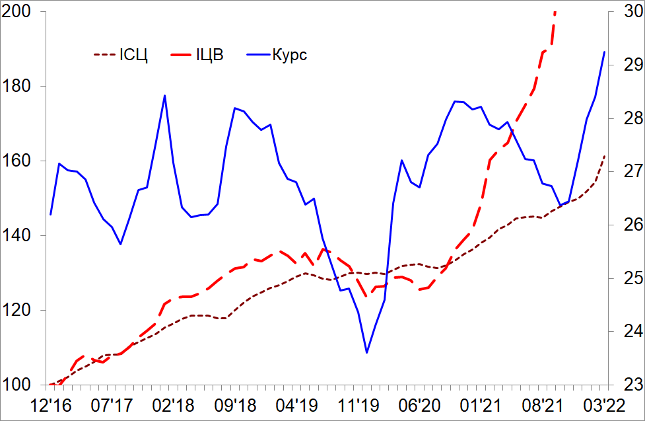

Inflationary dynamics in Ukraine is manifested in two ways. First, the change in the Consumer Price Index (CPI) is mainly caused by the change in the food price index, housing and utility tariffs, which are "regulated" administratively.

Second, exchange rate dynamics strongly influence producer prices (PPI), as shown by the increase in prices of energy imports. Usually, producer prices react quite briskly to currency shocks and outpace consumer prices, forming the so-called monetary overhang for consumer markets (diagram "Indices of producer and consumer prices and hryvnia exchange rate"), which may lead to consumer inflation.

Producer and consumer price indices (Dec. 2016=100) and hryvnia exchange rate (UAH/$1, right scale)

Exchange rate. PPI. CPI

So, the direct risks for Ukraine from the interest rates increase by the central banks of partner countries, as well as strengthening of the dollar on international markets, are not so grave yet. However, there is a reason for concern. It depends on how quickly the leading partners will be able to withstand the crisis (primarily, in Europe).

The current deterioration of the situation in national economies exhausts the resources which may be used to support partners. At the same time, on the one hand, there is growing "fatigue" from the need to tighten the belts, and with it, doubts about the expediency of helping others, especially in the long term. On the other hand, political confrontation is intensifying around not only the conditions for providing aid to a country that needs it, but also the expediency of continuing the sanctions policy against the aggressor, the consequences of which are among the important factors of the crisis, or the deterioration of the living standards.

Thus, Ukraine is interested in mitigation of crisis in general and inflationary threats in particular for its key partners (primarily, the EU), being a significant factor of further partner support, so needed by the country.

https://razumkov.org.ua/statti/znovu-pro-protsentnu-stavku-ta-infliatsiiu