")

")

On November 24, 2022, it will be 9 months of full-scale Russian aggression. Ukraine lost thousands of lives, hundreds of cities and villages were destroyed, business suffered irreparable damage, and the social security system was torn apart. Despite the hostilities that continue in the East and South, Ukraine, thanks to support from international partners, managed to keep the country's economy from collapsing, and in the autumn months it shows, albeit shaky, positive signs of stabilisation. The Ministry of Economy published an estimate of Ukraine's GDP decline in 9 months - about 30%. This (in the conditions of the war) may be considered a relatively good indicator (since in spring, estimates were as high as 40-50%).

We dare state that in autumn, the Ukrainian economy somewhat recovered. Here, we will provide evidence of the economic environment improvement in the fall of 2022.

Foreign economic situation. Ukraine's economy is getting integrated in the global economy. The following global economic signs of this autumn, including those shaped by the war in Ukraine, deserve mention:

- very high inflation in the developed countries (including the USA and the EU) due to Russian actions in the energy markets, accompanied with high employment, which complicates an anti-inflationary policy;

- global strengthening of the dollar, which is caused by and accompanied with an increase in interest rates in the USA, prompts a further increase in interest rates in other countries (to prevent weakening of their national currencies), which impedes economic activity and economic growth;

- central banks have to step up anti-inflationary measures and tighten the monetary policy, which may have recessionary consequences for economies (including due to the rise in commodity prices);

- a decrease in economic activity in the leading countries of the world puts a downward pressure on emerging economies (including China), which discourages global business activity;

- in emerging countries, the situation is worsened by the outflow of capital to "safe havens" (first of all, to the US markets), which limits access to financial resources;

- although developed markets show signs of stabilisation, business and household expectations remain low.

These global factors have an impact on a small open economy, such as Ukrainian. In previous years, crisis manifestations on world markets led to significant socio-economic losses for this country. Now, thanks to the international community, the negative pressure on Ukraine can be eased, but this will depend on the position of the world community, primarily the most powerful countries.

In the first half of November, three events took place almost simultaneously and had an impact on the situation in the world and in Ukraine.

The first one - mid-term elections in the USA, expected to influence economic, financial, and military aid to Ukraine. There was concern about a possible reversal of the US support policy for our country. However, it did not happen. At the same time, we can expect stricter control of the use of financial and military aid. Ukraine needs to demonstrate its transparency.

The next important event was the G19 summit, which was expected to give some answers to the questions of the day. We expected to hear about the convergence of the positions of the US and China regarding the war in Ukraine, and the assistance of world leaders to Ukraine. In this context, the summit in Bali was rather disappointing for Ukraine. The Ukrainian issue was not central for the US, China, or most participants. China often takes a far from pro-Ukrainian position, primarily in matters of dealing with the Russian aggression.

Simultaneously with Bali, the UN General Assembly adopted a resolution on a register of damages caused to Ukraine by the Russian aggression. Although the General Assembly ruled that Russia should be held accountable, it was another political declaration with little practical meaning. What is more disappointing for Ukraine is that China was among the 13 countries that voted against it. Other large emerging member countries of the G19 (Brazil, India, Indonesia, Saudi Arabia) abstained.

The improvement of the US-Chinese relations, which is likely to happen after Bali, does not mean that the circle of those who support Ukraine will expand. For Ukraine, this is also a warning signal. In no case should we try to return to attempts of implementing a "simple" model of partnership – the US as the political partner, and China as the economic partner #1 – which was promoted by some in the domestic political elite.

Assessment of economic activity. So far, there are no official data of the economy development. Expert studies are the only indirect (relatively reliable) source.

In November, 2022, the State Statistics Service published the results of its research of expectations of industrial enterprises in the 4th quarter. They were better than in the previous quarter. The indicator of business confidence in the industry increased compared to the 3rd quarter of 2022 by 2.4 percentage points and made –14.8%, in the processing industry, it equalled –13.6%. The business climate in industry improved by 0.6 percentage points, –1.5%, in the processing industry it increased by 0.8 percentage points, to –1.3%.

Somewhat different results are presented in the NBU study. According to the National Bank of Ukraine survey, deterioration of the security situation gave rise to negative expectations of businesses – the Index of Expectations of Business Activity in October was 44.9 (46.1 in September). Meanwhile, there is reason to believe that improvement of air defence will mitigate those risks.

Significant positive expectations of economic recovery are associated with decisions on "visa-free energy" (the domestic energy system has become an integral part of the European one), "visa-free economy" (exemption of Ukrainian products from all tariffs and quotas), "visa-free transport" (liberalisation of road traffic), "visa-free customs" (integration of Ukrainian customs with the European). Exporters expect positive "shift" due to the improvement of transportation, including exports by sea (the "Grain Initiative") and by rail.

However, new risks emerged and can slow down the recovery: massive bombing of critical infrastructure, first of all, intended for life support - electricity, water and heat supply (especially alarming before winter).

In November, Ukrainian cities and villages switched to metered electricity supply, emergency shutdowns became "common". In addition to inconveniences for households, long-term electricity outages affect productivity of industrial enterprises and household services.

Self-assessment of economic standing by Ukrainians. Support of Western partners continued, not only in the military or economic spheres but also social and humanitarian, so, the people do not panic. Despite huge losses, the current socio-economic state of Ukraine, as seen by the country citizens, is not a collapse.

The probable reason is that the authorities enjoy support of the country citizens. In order to repulse the aggressor, there appeared a conscious and voluntary unity of citizens, balanced centralisation of governance, subordination of all political and economic interests to a single goal - the most effective fight against the aggressor, which also contributed to the improvement of well-being.

According to the Razumkov Centre polls, the current well-being (self-assessments of households) does not differ much from what we saw before the war (table "Assessment of family well-being").

Assessments of family well-being, % of responses

|

|

05'21 |

09'22 |

11'22 |

|

Very bad |

10.4 |

10.5 |

10.7 |

|

Rather bad |

25.5 |

28.1 |

27.6 |

|

Very bad + rather bad |

35.9 |

38.6 |

38.3 |

|

Neither bad nor good |

47.6 |

49.5 |

45.4 |

|

Good |

13.0 |

8.5 |

12.0 |

|

Very good |

0.9 |

1.1 |

1.2 |

|

Good + Very good |

13.9 |

9.6 |

13.2 |

|

Hard to say |

2.6 |

2.3 |

3.1 |

|

Balance (positive - negative) |

-22 |

-29 |

-25.1 |

Of course, the estimates for September 2022 look worse than in peaceful May 2021, when the country practically got rid of the worries of coronavirus. However, estimates in November 2022 are much better than in September.

The absence of panic is witnessed by the increase of monetary resources and savings of households. The NBU data indicate the continued growth of deposits in hryvnias and foreign currency. On November 1, household deposits reached record-high UAH 954 billion. Such a trend is associated with large payments to the military, and with "currency liberalisation" - the opportunity to buy non-cash currency in banks and place it on term deposits for at least 3 months, and to convert hryvnias (unlimitedly) into term currency deposits. Both instruments are aimed to protect household savings from exchange rate fluctuations and high inflation.

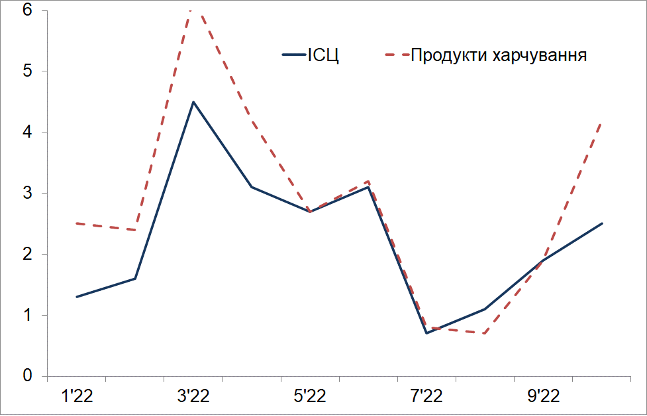

Since the well-being depends on purchasing power, a decrease in inflation will naturally give households confidence in improvement of the situation. Unfortunately, as the consumer price index strongly depends on the food price index (“Inflation in Ukraine” chart), the inflationary component will be significant at least until the spring of 2023 (due to the high dependence of processing industries on the cost of imported energy resources). Although the main price shocks already occurred in the spring of 2022, and there were reasons to hope for a decrease in inflationary pressure in 2023, a new wave of destruction of critical infrastructure by the Russian aggressor may restore inflationary threats.

CPI Foodstuffs

Foreign assistance. It would have been much more difficult for Ukraine to cope with aggression on its own. The international (democratic) community provides significant economic, military, and humanitarian support to Ukraine. Since the beginning of the war, financial aid (grants and loans) from international partners have amounted to $23 billion (US - $8.5 billion, EU - $4.8 billion). In addition to financing the budget deficit and repaying debts, they made it possible to keep international reserves in excess of $25 billion (3-4 months of future imports).

According to IMF estimates, in 2023 Ukraine needs about $3.5 billion monthly to provide basic services to the population and support the economy. Developed countries are expected to be the main financial donors. However, the IMF itself does not hurry to provide financial assistance. On October 17-20, the IMF mission met representatives of the Minister of Finance of Ukraine and the NBU head in Vienna to discuss current and future macro-financial indicators, the 2023 budget and related external financing needs, financial sector issues and strategies to support macroeconomic stability. Both sides expressed "satisfaction", but the NBU head confirmed that it was "still inappropriate and premature" to talk about the results. Such a "dualistic" position of the IMF is not surprising, Ukraine will have to live with it.

Meanwhile, Ukraine signed a Memorandum of Understanding on suspension of payments for state and state-guaranteed debts with a group of official creditors of Ukraine from the G7 countries and the Paris Club in order to mitigate the economic consequences of the Russian aggression (suspension of debt repayment from 08/01/2022 until the end 2023). The total amount of debts covered by this Memorandum is about $3.1 billion.

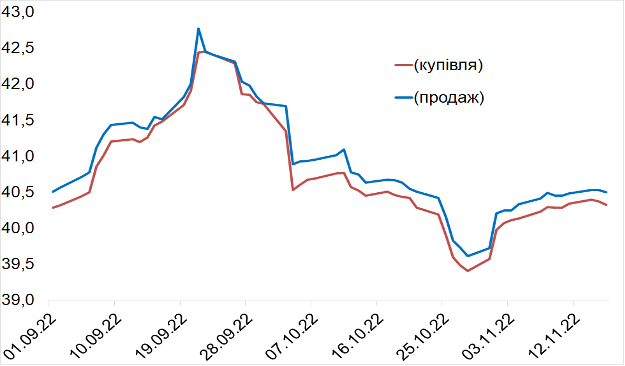

Exchange rate dynamics. In autumn, a noticeable weakening of the devaluation pressure on the hryvnia was observed. After the exchange rate shock in mid-September (the cash rate exceeded UAH 42.5/$1), so that the NBU had to perform massive interventions, over the next two months the hryvnia went up a bit and has recently fluctuated around UAH 40.5/ $1, that is, rose by 1.5-2 hryvnias per dollar.

Hryvnia exchange rate on the cash market, UAH / $1 (Purchase Sale)

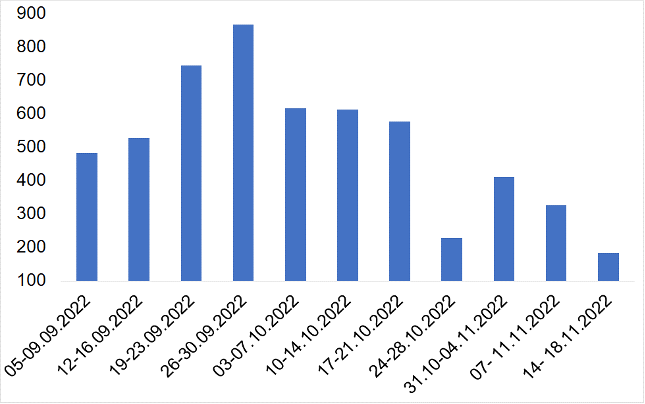

NBU interventions, $ million

This may indicate weakening of the psychological factor (fear of a new escalation of the aggression, including as a result of mobilisation, which might be one of the main factors of the September devaluation shock). Also, hryvnia’s strengthening in October took place in the conditions of intense bombings.

Of course, such positive dynamics were associated with NBU interventions to support hryvnia (diagram "NBU interventions"). At the same time, the NBU had to use reserves, which was made possible by the extensive financial support of the partner countries. In autumn, the NBU carried out interventions worth $5.5 billion, and from the beginning of 2022 till the end of November, the NBU bought $3.2 billion and €111 million and sold $22.4 billion and €1.8 billion in the interbank market.

Recently, there have been renewed proposals for a stronger linkage of the hryvnia to the euro (instead of the US dollar), due to Ukraine’s policy of European integration. However, it seems premature. Although trade between Ukraine and the euro zone countries indeed goes up, the historical and psychological attachment to the dollar is significant. The weakening of the euro against the dollar, which occurred this year (and is likely to persist in the next year due to the much higher interest rates in the USA), calls into question the feasibility of such a turn, at least in the medium run. Since the reserves, debts, foreign currency deposits of the population, international aid (including lend-lease) are mainly denominated in dollars, all this makes dollar strong in Ukraine. Attempts to intervene in the currency environment (especially in wartime) do not look reasonable.

Some generalisations and predictions.

- The autumn of 2022 turned out to be hard for Ukraine in the international environment. Leading developed countries (the USA, Great Britain, the EU, Canada, Japan, etc.) continued to support Ukraine economically and militarily. It may be argued that despite the election processes and government changes (in the USA, Italy), comprehensive aid to Ukraine will continue and, probably, even grow.

Unfortunately, China, as one of the influential global leaders, seems to distance itself from the war in Ukraine. The improvement of relations between the USA and China, which will probably take place after Bali, does not at all mean that the circle of those (emerging countries) who support Ukraine will expand. Hence, Ukraine should double its efforts to better inform the leading emerging countries (members of the G19, the Gulf states, ASEAN) about itself, the war, and its economic potential.

Ukraine’s struggle against the Russian aggression has clearly demonstrated that the military success of the AFU has a direct impact on Ukraine’s image in the world, the scope of military and economic aid provided by partner countries. Taking into account the slow but steady changes in the nature of hostilities, liberation of vast occupied territories, the flow of those who return to Ukraine, one may expect further strengthening of partnership and more active involvement of Ukraine in the civilised world.

- While the success of the AFU is a strong positive factor for Ukraine’s economic recovery, deterioration of the security situation in the country leads to negative business expectations of economic activity. This is confirmed by various expert studies in connection with the intensification of Russian bombings and destruction of critical infrastructure facilities, primarily related to the livelihood of the population - electricity, water supply, heating (which is especially relevant in winter).

Meanwhile, there are grounds to assert that the strengthening of air defence will reduce the mentioned risks and thus contribute to positive expectations of domestic businesses.

An additional factor for Ukraine’s economic recovery may be presented by the decisions adopted in summer and autumn on "visa-free energy", "visa-free economy", "visa-free transport", "visa-free customs", which will contribute to the expansion of international trade and Ukraine’s integration in the European networks.

- Since the consumer price index strongly depends on food prices, the inflationary component may remain strong in Ukraine at least until the spring of 2023. Although the main price shocks in the country already occurred in the spring of 2022, and there were reasons to hope for a decrease in inflationary pressure in 2023, a new wave of destruction of critical infrastructure by the Russian aggressor may restore inflationary threats.

While in wartime, high inflation is not surprising for Ukraine, and the well-being depends on the purchasing power, the reduction of inflationary pressure will give households a hope for the better. Thus, the reduction of threats to the critical infrastructure will be a stabilising factor of the socio-economic situation in Ukraine.

- In autumn, the Ukrainian financial and banking systems continued to function steadily, which even allowed the NBU to take some foreign exchange liberalisation measures. Of course, exchange rate dynamics remained sensitive to external troubles, but after the exchange rate shock in mid-September, which the NBU "extinguished" with massive interventions, over the next two months the hryvnia even rose, which reduced the imported inflationary pressure.

Such positive exchange rate dynamic was associated with significant NBU interventions to support hryvnia: in autumn, the NBU made interventions worth $5.5 billion. For this, the NBU had to use reserves, which became possible thanks to the extensive financial support of partner countries. During the war, the financial aid (grants and loans) from international partners totalled $23 billion (US - $8.5 billion, EU - $4.8 billion), which made it possible to maintain gross international reserves at a level of more than $25 billion (3-4 months of future imports).

According to IMF estimates, in 2023 Ukraine will need about $3.5 billion per month to provide basic services to the population and support the economy. So far, Ukraine's negotiations with the IMF on a large-scale program remain inconclusive, and the IMF itself is in no hurry to provide financial assistance. Thus, it remains to be hoped that the leading developed countries will remain the main financial donors of Ukraine. Until now, their promises have been firm and effective.

See the full article in Ukrainian at: https://razumkov.org.ua/statti/ekonomichni-oznaky-ta-osoblyvosti-oseni-2022r