")

")

In one of our previous policy papers we pointed out the risks of a gradual but steady slide of the world's leading economies into negative economic dynamics, which will certainly affect the world economy in general. For Ukraine, this may have a double negative impact - on the one hand, a decrease in aggregate demand, and a resultant decrease in the demand for its export products, on the other hand, a decrease in the resources that partner countries can use to support Ukraine. Unfortunately, negative signals of the slowdown of the leading economies continue to appear.

Weakening of business activity in the USA and Europe. The US and the EU remain global economic centres that largely determine the dynamics of the world economy. Therefore, their economic dynamics remain in the focus of attention.

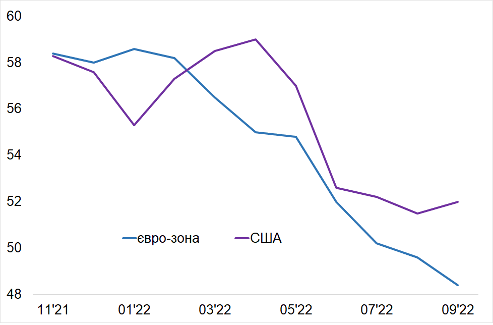

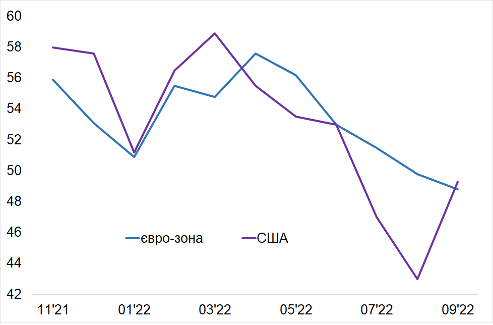

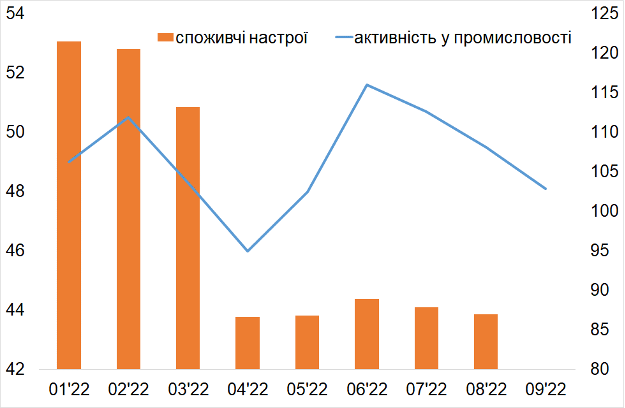

Since the beginning of the year, said global centres have shown downward trends both in industry and in the service sector (diagram "Business activity..."). A greater decrease in economic activity indicators in the euro zone (compared to the USA) is mainly due to the crises in the European energy markets caused by Russia, as an element of its hybrid war against the EU, and some measures of the sanctions policy, for which, some EU countries initially were not ready. Since the downward trend in business activity has been lasting for several quarters, the risks of a global recession and subsequent depression of the leading economies are growing considerably.

Business activity in the manufacturing and service sectors of the USA and the Eurozone, indices

Processing industries

Service industries

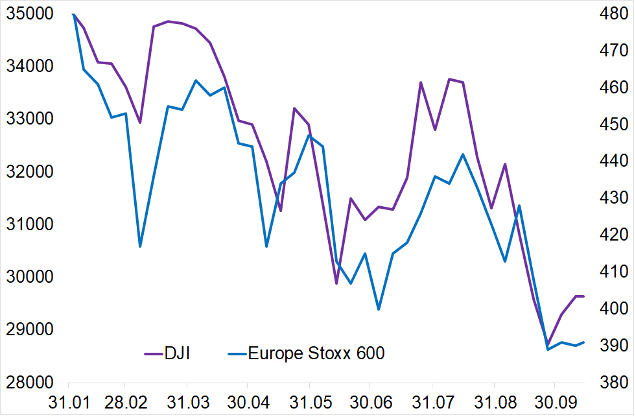

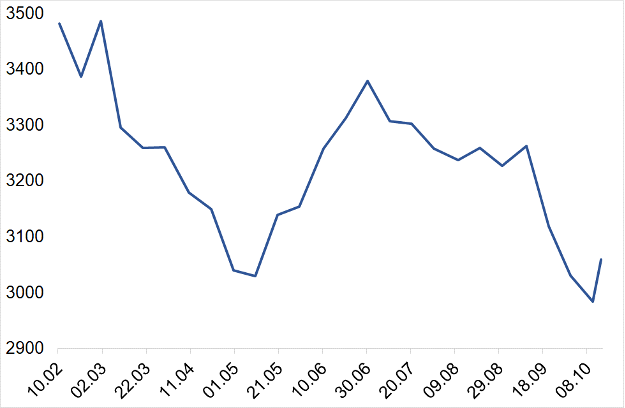

Economic troubles are confirmed by the (negative) dynamics of the most important stock indices, as an indicator of the financial well-being of the largest companies and corporations that determine the "quality" of the business environment in developed countries. In 2022, the Dow Jones Index in the USA and the index of the largest companies in Europe (STOXX 600) experienced two waves of a sharp decline. The first of them (in the spring) was partly related with the sanctions policy and the relevant imbalances in commodity markets and logistics chains. The second one, which has accelerated since August, is rather related to interest rate raising by central banks, which is considered a necessary element of the anti-inflationary policy (chart "Stock indices in the USA and Europe")

Stock indices in the USA (DJI, left column) and Europe (right column)

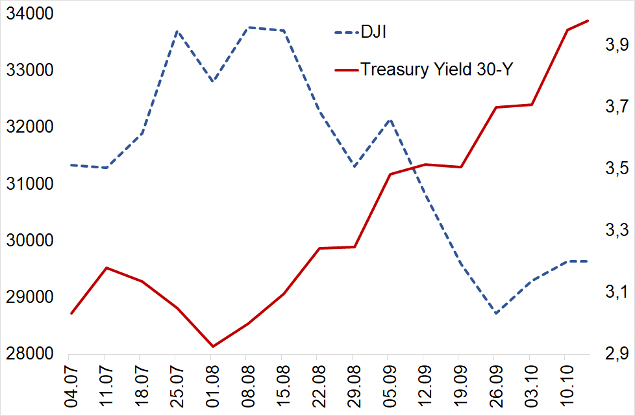

We have already pointed out that countering inflation through the increase of central banks' base rates does not appear to be unconditional, since it limits economic recovery and development. Moreover, higher rates bring specific macroeconomic complications and troubles.

Thus, following the rates (in the conditions of poor business activity), the yield of government bonds and other debt instruments increases (chart "Dow-Jones Index and the yield of long-term US bonds"), which makes new borrowings more expensive (including for repayment of the old “cheap” obligations), and therefore, the risks of bad debts increase. The resulting circle of mutual negative influences (if sustained for a long time) will also push the leading economies into depression.

The Dow Jones index (left side) and the yield on long-term US bonds (right side)

The Chinese factor. Another important factor for the deterioration of the situation in the global economy is presented by the recession in China. In the 2nd quarter of 2022, the seasonally adjusted indicator of economic growth showed a decrease of 2.6%, for the first time after the coronavirus shock in the 1st quarter of 2020. Moreover, the factors of recession in China differ from European or American ones and are both internal and external in nature.

There are reasons to claim that in 2022 China stays under the influence of at least two negative waves. The first wave is financial, which began in the summer of 2021, when the second largest Chinese development giant Evergrande announced a possible bankruptcy. This caused a payment crisis, growth of arrears and debts not only in the construction industry but also in the banking sector, which, in turn, worsened the loan conditions of the real sector in general, and with that, affected economic dynamics.

The second wave — socio-political — is connected, on the one hand, with the attempts of the Chinese leadership to achieve a "zero" shock from the second coronavirus wave (as one of the priorities of the domestic policy). In March-April, when strict coronavirus restrictions reappeared, economic troubles "naturally" resumed. In particular, the consumer sentiment, after collapsing in the spring months, did not recover until autumn (chart "Business activity and consumer sentiment in China"). Business activity, which partially recovered in the summer months after the spring shock, has again been showing downward trends since the beginning of September (Shanghai Stock Exchange Index chart)

Business activity (left panel) and consumer sentiment in China (right panel), indices

Shanghai Stock Exchange index

The other aspect of the negative waves that inhibit economic recovery in China is presented by the political factor, primarily related to the confrontation with the United States, including over Taiwan, as well as the differences between the US and China regarding the war in Ukraine. A common feature of these confrontations is that Ukraine and Taiwan, as democratic countries that historically chose freedom and independence, are fully supported by developed countries. China has to reckon with this.

This political factor will persist. However, international experts speculate that if the two world leaders meet at the G20 summit in Bali, it will be an important signal of a possible rapprochement. At least, the National Security Strategy presented on October 12 admits that the United States should cooperate not only with developed democracies to strengthen its leadership in solving global problems.

Conclusions for Ukraine. According to a number of international experts, the risk of a great global "stagflation" characterised by instability and periodic various negative shocks is growing. At the same time, even a slight positive shift in relations between the US and China can become a significant factor reducing economic risks.

In such conditions, where each country has to overcome crisis phenomena, mutual understanding will be complicated, which, in turn, may weaken attention to the needs of the country resisting an aggression. So, Ukraine is highly interested in the soonest improvement of relations between the US and China.

In the case of such improvement, we may expect a more adequate attitude of China to the Russian aggression, which, given China’s weight in emerging countries, will contribute to a better positioning of Ukraine in the world community (not only in democratic countries).

It can also bring considerable economic benefits to Ukraine, not contrary to the ideological and political priorities of the country. First of all, it is about the new role of the Belt and Road initiative (New Silk Way). The current route from China to Europe via Russia and Belarus has lost all prospects. However, China will persistently look for ways to the European markets. Ukraine can offer alternative routes, especially in the case of Ukraine's integration with the neighbouring EU member states. If it maintains strategic relations with the USA, risks of uncontrolled sale of domestic strategic enterprises, as it happened previously, will be minimal for Ukraine.

https://razumkov.org.ua/komentari/ryzyky-ekonomichnogo-spovzannia-zrostaiut