")

")

Yuriy Yakymenko, Razumkov Centre President

Vasyl Yurchyshyn, Economic Programmes Director

In Ukraine, 2022–2023 will go down in history as years of great trials and losses. Meanwhile, since the domestic economy for two years has shown impressive signs of stability in the conditions of long-term, large-scale Russian aggression and not only managed to preserve a great deal of its potential but (despite continued hostilities) but made the first steps towards recovery, this gives reason to cautiously assert that 2024 will bring further positive transformations of the domestic socio-economic situation, resulting in economic strengthening and improvement of well-being.

Along with this, the traditional caution should not be ignored. If the nation has demonstrated unity to repel aggression of an external enemy, this does not necessarily rules out serious challenges to its cohesion in the future. The history of Ukraine testifies that maybe the greatest losses of independence and freedom occurred when statist and patriotic forces failed to unite, lost the trust of their compatriots, thereby opening the way for revenge by anti-Ukrainian forces. Unfortunately, at the end of 2023, there is an increase in internal political tension, which, along with the difficult situation at the front and contradictions in some partner countries regarding further assistance to Ukraine, is causing disappointment of a part of society and concern of citizens about the future prospects of the country.

However, we believe that the coming year 2024 will be a good year for Ukraine. That is why this publication considers the scenario/forecast of the country's development in 2024, which, we believe, will correlate with the actual socio-economic developments.

1. Socio-political context of the country on the eve of 2024

First of all, it should be noted that the entry of Ukraine into 2023 was accompanied with another round of aggressive and provocative actions by the Russian invaders, which could not only bring additional economic losses but slow down the country’s recovery. We are talking about massive bombings (almost on a daily basis) of critical infrastructure, primarily related to the livelihood of the population — electricity, water and heat supply (which is especially relevant in the winter). Back in November 2022, Ukrainian cities and villages switched to metered electricity supply, rolling and emergency shutdowns became common. In addition to the inconvenience for households, long-term power cuts meant reduced operation hours of many industrial enterprises and almost the entire sector of household services.

It may seem strange, but the domestic economic environment quickly adapted to the new challenges. In 2023, production indicators showed improvement (albeit weak) and evidenced a gradual exit from the economic abyss into which Russia pushed Ukraine in 2022 (recall the real GDP drop by 30%). Which, by the way, was confirmed in 2023 by revised forecasts of Ukraine's economy development (by international institutions and governmental agencies) — from extremely low rates of growth (or even decline) of real GDP at the beginning of the year, to completely optimistic ones in the fall.

Say, in October, the World Bank raised its forecast of Ukraine's GDP growth in 2023 to 3.5%, which is 1.5 percentage points (p.p.) higher than its June estimate (at the year beginning, they even expected a decline). The main factors behind the improved outlook included more stable electricity supply, increased government expenditures, large foreign aid, a higher-than-expected harvest, and improved consumer and business confidence, which contributed to a gradual increase in activity in 2023, after a collapse a year ago.

Of course, the conditions for Ukraine’s economy development in 2024 will be determined by a tangle of multidirectional internal and external factors, which will be aggravated by international confrontations of major political and economic powers, preservation of high risks of continued full-scale Russian aggression, and new hotbeds of military confrontation. We do not ignore such risks, but in spite of them we maintain the position that the coming year 2024 will strengthen macroeconomic stabilization processes in Ukraine.

Among the likely (within certain limits, contradictory) processes that will contribute to impede macroeconomic recovery, we would like to note the following:

- Continued liberation of the Ukrainian territory, despite strong resistance of the invaders, which can make our liberation struggle longer. We do not consider the scenario of a quick end to hostilities on the territory of the country, nor do we consider the scenario of preserving hostilities and starting "peace talks";

- Partner military, financial and humanitarian assistance will continue, although it will be a bit smaller, and will mainly focus on military purposes. We do not consider a scenario of ending or minimizing foreign aid;

- Domestic political tension will not develop into a confrontation, institutes of power will continue to work in accordance with the Constitution and the effective legislation, civil society will remain active, provocative acts aimed at oppressing democratic rights and freedoms or causing public confrontation will be impossible;

- Reconstruction and restoration will be stepped up in the regions that were strongly affected by the invasion. The growth of economic activity will occur both as a result of extensive factors (economic activity in the liberated territories and the return of displaced persons to their homes (Kharkiv, Sumy, Chernihiv, Kherson regions)) and intensive factors (growth of the business activity in all regions that are becoming safer);

- Difficulties in access to external resources will lead to stronger devaluation and inflation, the alternative being the loss of reserves or a stricter fiscal and monetary policy (both of which contradict the objectives of development and growth). Complications may arise with payments under external obligations, the fulfilment of which will require the use of foreign exchange reserves. Therefore, devaluation of the hryvnia and associated inflation may turn out to be a better alternative, and according to our forecast, their levels will slightly exceed official expectations. Meanwhile, an increase in inflation may prove to be a relief for budget expenditures due to the nominal GDP growth.

- A decrease in external revenues means that the domestic debt will grow, which, however, is easier to refinance. At the same time, it will be necessary to resolve the contradiction — the government's needs to raise more funds will provoke an increase in bond yields, which will make debt servicing more expensive and ultimately have an extremely negative impact on inflation and the forex market.

2. Key macroeconomic indicators of 2023–2024

The collapse of the economy caused by Russian aggression in 2022 formed a very low base for comparison with the following years. Therefore, the high growth indicators of 2023–2024 should not be misleading — the country has not yet entered the trajectory of sustainable GDP growth. Meanwhile, if stabilization processes are started in 2024, the country may enter 2025 with strong positive expectations. We see preservation of the economic dynamics of 2023 in 2024 as a good basis for soonest recovery in the coming years.

This approach is confirmed by the forecast presented by the NBU in the latest inflation issue. Agreeing with the rationale of the provided forecast indicators and assumptions, we tend to see a slightly different (probably less optimistic) nature of the national economy development, based on the (preliminary) results of 2023. The main ideological difference between our 2024 forecast and the official one is a slightly lower level of real GDP growth, higher inflation, an increase in the foreign trade deficit and greater losses of foreign exchange reserves (due to the need for external and currency balancing) (table "Key macroeconomic indicators of 2021–2023 and forecast for 2024") (see the details below).

Key macroeconomic indicators of 2021–2023 and forecast for 2024

|

2021 |

2022 |

2023 |

2024 |

|||

|

|

NBU |

NBU |

NBU |

Razumkov Centre |

NBU |

Razumkov Centre |

|

GDP, UAH billion |

5451 |

5191 |

6625 |

6590 |

7730 |

8360 |

|

Real GDP growth, % |

3.4 |

-29.1 |

4.9 |

4.0 |

3.6 |

4.0 |

|

CPI growth, % (Dec. to Dec.) |

10.0 |

26.6 |

5.8 |

6.8 |

9.8 |

12.9 |

|

CPI growth, % (average) |

9.4 |

20.2 |

12.9 |

13.1 |

8.3 |

10.0 |

|

Balance of current accounts, $ billion |

-3.9 |

8.0 |

-7.3 |

-6.2 |

-11.0 |

-12.0 |

|

Gross NBU reserves, $ billion |

30.9 |

28.5 |

41.8 |

39.0 |

44.7 |

35.0 |

|

Growth of average nominal wages, % |

20.9 |

6.0 |

17.7 |

12.2 |

15.8 |

22.9 |

GDP growth and inflation. Our assessment of real GDP growth in 2023 remains unchanged and today is lower than in the NBU forecast (although the government’s initial growth forecast in 2023 was close to zero). The main factors behind our refusal to revise the forecast of the real GDP growth rate upwards include a certain deterioration of the dynamics of partner aid and the growing risks of resuming massive attacks on the energy infrastructure in autumn and winter. Of course, domestic energy companies now do have the experience in repairs, but this will slow down production activity and weaken incentives for soonest recovery.

Another factor behind our reluctance to raise the real GDP growth is the energy component — the expected acceleration of inflation in autumn and winter due to the increase in oil prices, caused by the coordinated cuts in oil production by Saudi Arabia and Russia. Of course, the energy crisis of 2022 will not repeat itself, but shock jumps in the cost of energy resources are quite likely, especially if the winter is cold and creates a significant demand for energy resources in households.

Regarding the development of the real sector, unfortunately, it should be admitted that such an important recovery tool, which was supposed to be the "Marshall Plan", and for which there were great hopes at the beginning of 2023, was not put into effect. To a large extent, the reason is that the Ukrainian government has failed to prepare a clear recovery programme (instead of a list of facilities, for the construction or reconstruction of which significant foreign funds are needed).

Another factor in the weakening of economic incentives for growth is the cross-border conflict between Ukraine and the neighbouring European countries related with exports and even transit of Ukrainian grain and foodstuffs, which, along with the end of the "grain initiative", will have a negative impact on production capacity and balance of payments.

Wages. Of particular interest is the assessment of the level of wages, due to the fact that from the beginning of 2022, the State Statistics Service does not provide information on average wages. Their value is obtained indirectly, through the calculation of pensions in the Pension Fund. According to these data, the average wages remained stagnant, while payments to the military increased rapidly. Although this had little effect on the average indicators, in 2022 household deposits increased sharply.

At the same time, the economic revival was reflected in wages, which began to rise noticeably from the spring of 2023. Moreover, given the slowdown in inflation, the real purchasing power of wages also grew. Since our expectations are related with further stabilization of the macroeconomic situation and growth of demand for skilled labour, there are reasons to expect accelerated growth of wages. According to our estimates (box "Estimation of nominal average wages"), the average nominal wages will increase by more than 12% in 2023 and reach UAH 16.7 thousand; in 2024, they will increase in nominal terms by 23% (according to the NBU forecast — by 16%) and will reach UAH 20.5 thousand (table "Key macroeconomic indicators of 2021–2023 and forecast for 2024").

We stress that strengthening of the country's defence and economic capacity in 2024 means that in this period the demand for labour may increase rapidly, and in the conditions of the shortage of manpower (military, migrants), employers will be ready to raise wages significantly, which, in turn, may encourage Ukrainians to return from abroad (and will become a significant factor of economic recovery and GDP growth).

However, the demand will grow specifically for skilled labour, for those workers who have already proven their ability or are ready for new competitive conditions, and employers will be ready to significantly raise wages to such workers. The reverse side of such a "format" of demand is that the unemployment rate in 2024 will practically remain at the level of 2023.

ESTIMATION OF NOMINAL AVERAGE WAGES

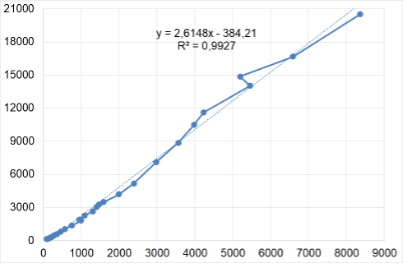

We used two methods for the assessment of wages. The first one is based on the fact that since wages make approximately half of the nominal value of the created product, the dynamics of wages quite clearly correlates with that of nominal GDP, and the formed relationship is quite stable. Indeed, domestic practice and statistics confirm this (diagram "Nominal GDP and nominal average wages").

Nominal GDP (billion UAH, horizontal axis) and nominal average wages (UAH, vertical axis)

The second one rests on job seekers' requests (in their CVs) and the corresponding wages (offered by employers). Work.ua is s popular web site where job vacancies and search queries are posted, where a large amount of information is collected. Usually, requests are ahead of the wage levels offered to job seekers but may serve as a reference point for likely changes in the near future.Moreover, the dynamics of wages based on CVs has a stable enveloping nature for actual wages, and shows a clear upward trend with signs of acceleration from the summer of 2022. So, it indicates that the average wages in 2023 will be UAH 16.3 thousand (corresponding to the previous estimate), and the closest short-term benchmark is UAH 18,000 (diagram "Average wages and CV demands").

Average wages and CV demands, UAH

▬ nominal average ▬ vacancies’ web site

3. Monetary basis for recovery

Credit should be given to the National Bank of Ukraine, which managed to maintain monetary stability despite aggression, and the banking system ensured the functioning and preservation of public funds. The rational foreign exchange policy was an important stabilizing factor of the entire economic environment, which allowed for a weak devaluation of the hryvnia, reducing the risks of washing out reserves and capital flight, and also contributed to the partial balancing of demand and supply of currency on the cash markets.

Exchange rate arrangements change. On October 2, 2023, the National Bank took a bold and long-awaited step — it finally publicly abandoned the policy of inflation targeting and announced transition from a fixed exchange rate to the so-called "managed exchange rate flexibility" regime. This means that the NBU does not allow the hryvnia to "float freely", plans to continue its support, but at the same time allows the exchange rate to respond to certain market trends. In particular, the regulator is ready to sell gold and foreign exchange reserves, satisfying excessive demand for dollars in order to prevent sharp fluctuations in the exchange rate. Transition to the new regime was a step towards currency liberalization and return to the pre-war regime of the currency market.

It should be noted that expectations of some tension and growth in demand for foreign currency have partially come true, since more foreign currency is leaving Ukraine than entering the economy (due to the foreign trade deficit, a decrease in revenues from labour migrants, and an increase in the expenses of Ukrainian emigrants abroad). However, for the time being, the NBU's foreign exchange reserves are sufficient to prevent shock exchange rate fluctuations, and the assistance of partner countries allows replenishing those reserves.

The risks for exchange rate dynamics are related to the fact that if the military situation worsens or partner aid decreases, then a rapid increase in demand for foreign currency, and with it — an increase in devaluation tendencies or the loss of reserves, will become likely.

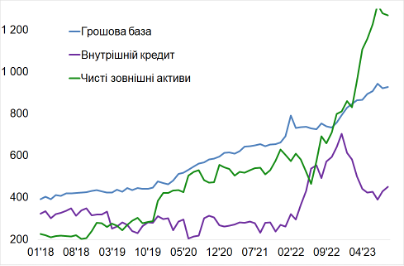

Monetary aggregates. The importance of partner assistance for formulation of a balanced monetary policy is evidenced by the fact that starting from the spring of 2022, the monetary base was formed precisely thanks to the resources of the partner countries, which came in the form of grants or budget financing (diagram "Components of the monetary base"). Note that a similar situation (albeit on a much smaller scale) occurred in 2020, during the coronavirus pandemic.

Therefore, it became possible to abandon rather strict monetary restrictions (in particular, due to the high discount rate) and to start successive steps towards monetary expansion — a necessary condition for the growth and strengthening of the real sector of the economy. The continuation of such support, we believe, will lead to an accelerated supply of money. So, while in 2024 the NBU expects the monetary base to grow by 16.2%, and the mass — by 13.0%, according to our scenario, the growth of those aggregates will make 19.9% and 19.4%, respectively (table "Main monetary aggregates"), which may result in higher inflation.

At the same time, lending to domestic economic agents will recover extremely slowly, due to the persistence of high risks. Say, loans to residents in 2024 will grow by meagre 5-6% (in 2023 — a decrease by 1–2%), i.e. (due to inflation) real money balances will continue to decrease. "Caution" in lending kind of runs contrary to deposits of businesses and households. The latter are under no less pressure of uncertainty, but continue and will continue to entrust funds to the banking system. The rate of growth of household deposits will significantly exceed the rate of inflation, which means the growth of real funds on household deposits (table "Household deposits and loans").

Components of the monetary base, UAH billion

▬ Monetary base

▬ Domestic credits

▬ Net foreign assets

Main money aggregates (end of period)

|

|

2021 |

2022 |

2023 (estimate) |

2024 (forecast) |

|

Monetary base, billion UAH |

662.5 |

792.5 |

960.0 |

1200.0 |

|

growth to the previous year, % |

11.2 |

19.6 |

21.1 |

19.9 |

|

Growth of cash in circulation, % |

12.6 |

14.6 |

14.1 |

15.8 |

|

Monetary supply, trillion UAH |

2.1 |

2.5 |

2.95 |

3.7 |

|

Monetary supply growth, % |

12.0 |

20.8 |

24.0 |

19.4 |

|

М2 circulation velocity |

2.8 |

2.3 |

2.4 |

2.5 |

|

Growth of consumer price index (Dec. to Dec.) |

10.0 |

26.6 |

9.8 |

12.9 |

Household deposits and loans (end of period)

|

|

2021 |

2022 |

2023 (estimate) |

2024 (forecast) |

|

Household deposits, billion UAH |

794.2 |

1045.7 |

1200 |

1450 |

|

Growth of household deposits, % |

8.7 |

31.7 |

14.8 |

20.8 |

|

Household deposits as % of GDP |

14.6 |

20.1 |

18.5 |

17.6 |

|

Household deposits, $ equivalent |

29.2 |

28.6 |

30.8 |

33.3 |

|

Household loans, billion UAH |

254.4 |

221.1 |

240.0 |

260.0 |

|

Growth of consumer price index (Dec. to Dec.) |

10.0 |

26.6 |

9.8 |

12.9 |

4. External sector — balance of payments and debts

Despite the ongoing aggression and noticeable complication of Ukraine's relations with some foreign partners, we maintain optimistic expectations that in 2024 it will be possible to start systematic international programmes for the recovery of Ukraine, although their implementation will have contradictory effects on the balance of payments. First, it will lead to a significant increase in the import of goods and services to cover consumer needs and the needs of project implementation, which will lead to an increase in the foreign trade deficit and put pressure on the exchange rate and the country's debt. Secondly, the inflow of (investment) capital will intensify (however, it will remain moderate), which will finance part of the trade deficit and relieve the debt pressure.

Balance of payments — current accounts. Ukraine entered 2023 with significant "distortions" in the balance of payments. Say, in 2022, the deficit of foreign trade (in goods and services) exceeded $25 billion, and the surplus of current accounts was record high over the past 10 years: $8 billion, due to the high inflow of primary (largely, salaries paid by foreign employers) — $8.5 billion — and secondary (partner assistance) — $25 billion — incomes.

Export losses in 2022–2023 mainly occurred due to the virtual destruction of the industrial (including metallurgical, which remains of critical importance for export) potential in Dnipropetrovsk, Kharkiv, Donetsk and Mykolaiv regions, which is still far from being partially restored. Probably, this export group will not regain its position in the structure of domestic exports, at least without significant structural changes and large-scale investments in advanced metallurgical technologies (without which it is difficult to hope for strengthening the country's export capacity, at least in the medium term).

The "distortions" continued in 2023 and will probably be observed in 2024. That said, exports will continue to decrease, while imports will increase (table "Foreign trade"), which will lead to an increase in the foreign trade deficit. However, thanks to the nominal GDP growth and weak devaluation, the deficit in the structure of GDP will decrease from (estimated) 21% in 2023 to 18% in 2024.

Foreign trade

|

|

2021 |

2022 |

2023 (estimate) |

2024 (forecast) |

|

Export of goods, $ billion. |

63.1 |

40.9 |

33.0 |

35.0 |

|

Export of goods and services, $ billion. |

81.5 |

57.5 |

50.0 |

52.0 |

|

Export of goods and services, % of GDP |

40.8 |

35.9 |

29.6 |

26.4 |

|

Import of goods, $ billion. |

-69.8 |

-55.6 |

-59.0 |

-63.0 |

|

Import of goods and services, $ billion. |

-84.2 |

-83.3 |

-86.0 |

-88.0 |

|

Import of goods and services, % of GDP |

42.2 |

52.0 |

51.0 |

44.8 |

|

Rate of coverage of imports with exports (goods and services), % |

96.8 |

69.1 |

58.1 |

59.1 |

|

Balance of foreign trade in goods and services, % of GDP |

-1.4 |

-16.1 |

-21.0 |

-18.0 |

Precisely thanks to the partner aid (inset "US Aid to Ukraine") in 2022–2024 it was and will be possible to keep the current accounts of the balance of payments within "acceptable" limits (table "Balance of primary and secondary incomes and current accounts"). The volume of such revenues will significantly decrease in 2024, which is an additional incentive for the Ukrainian government to step up transformations, so that despite the military risks, the attractiveness of investing in Ukraine will gradually grow.

US AID TO UKRAINE

During the 18 months of the war, from February 24, 2022 to July 31, 2023, Ukraine received $60.2 billion in the form of grants and preferential loans/guarantees. Of this amount, $32.1 billion was received in 2022. The USA, the EU, the IMF, Canada and the World Bank provided 83% of the total amount.

According to the US Council on Foreign Relations, the US sent a total of $78 billion in humanitarian, financial, and military aid to Ukraine:

- $26.4 billion — financing the budget of Ukraine from the Economic Support and Loan Fund;

- $23.5 billion — the cost of weapons and equipment delivered from the stocks of the US DoD;

- $18.3 billion — spending on military training, logistical support and other assistance under the Ukraine Security Assistance Initiative of the US DoD;

- $4.7 billion — grants and loans under the Foreign Military Aid Program;

- $3.9 billion — humanitarian aid, which includes food, medicines, and support for refugees.

These are unprecedentedly high figures and, to a large extent, thanks to them Ukraine managed and continues to resist the Russian aggressor.

In the fall of 2023, the United States will continue to provide financial support to Ukraine on a regular basis, including through the Multi-Donor Trust Fund of the World Bank.

Balance of primary and secondary incomes and current accounts

|

|

2021 |

2022 |

2023 (estimate) |

2024 (forecast) |

|

Balance of primary incomes, $ billion. |

-5.8 |

8.5 |

6.8 |

6.0 |

|

Balance of secondary incomes, $ billion. |

4.6 |

25.2 |

23.0 |

18.0 |

|

Balance of primary and secondary incomes, $ billion. |

-1.2 |

33.7 |

29.8 |

24.0 |

|

Balance of foreign trade in goods and services, % of GDP |

-1.4 |

-16.1 |

-21.0 |

-18.0 |

|

Balance of accounts, % of GDP |

-2.0 |

5.0 |

-3.6 |

-6.0 |

|

Balance of accounts, $ billion |

-3.9 |

8.0 |

-6.2 |

-12.0 |

The initiatives of foreign partners can play an important role here, which will have a decisive influence on investments growth in Ukraine in the near future. Say, France presented a bilateral insurance mechanism for its companies (state insurance company Bpifrance Assurance Export), which are ready to invest in Ukraine and participate in the country reconstruction before the end of the war. Firstly, it opens up opportunities for foreign (French) companies to invest in Ukraine, despite the continued hostilities. Secondly, it minimizes the risks of losing investments from France, as the insurance is provided and guaranteed in accordance with the French legislation.

Another long-awaited important step was taken by Belgium, the first of the EU countries. Its government created a special fund to support Ukraine in the amount of €1.7 billion, filled with taxes of the profits on Russian assets frozen in that country. Currently, there are no agreed mechanisms for the use of frozen Russian assets to the benefit of Ukraine within in the EU as a whole. If other countries manage to invent and implement similar mechanisms, Ukraine may receive significant resources for recovery (which will certainly improve the balance of payments and the debt position).

The next course of action, which looks very promising, is being tested today. The thing is that the development of the logistical infrastructure on the western borders of Ukraine (and with it, the formation of the potential for the production of technological goods with the participation of companies from partner countries) may slow down (which, in turn, will slow down cross-border trade in services).

The reason (or pretext) for the conflict that arose in the summer of 2023 is associated with the export (and transit) of Ukrainian grain and certain foodstuffs to the EU — in July, Poland, Bulgaria, Hungary, Romania and Slovakia agreed a general declaration that prohibited imports Ukrainian grain to those countries. Although the European Commission partially supported Ukraine, the conflict was not over. Later, the parties took steps to rapprochement (and the "degree" of the conflict went down), but Ukraine is most of all interested in a proper compromise solution and cannot afford confrontation with the neighbouring partners. Utmost avoidance of misunderstandings provides grounds for the successful economic integration of Ukraine in the EU.

Debt. At the beginning of 2022 fairly high macroeconomic risks were associated with Ukraine's foreign debt. However, in the future these risks were localized, including thanks to the assistance of partner countries.

In this context, it makes sense to remind of another feature of the foreign debt policy — successful restructuring of payments, including the easing of payments conditions for some debts in 2022. Although relatively small amounts were saved, the government demonstrated a skillful approach to foreign debt problems, which, by the way, bears an important sign for partner countries. In 2023, Ukraine’s debts were mounting. We only refer to the external governmental debt, since the internal debt is easily covered and refinanced (in the end) by the NBU.

The debt situation in Ukraine remains among the most difficult, and there are reasons to claim that the country's external public debt will exceed the financially critical level of 60% of GDP by the beginning of 2024 (Table "Ukraine's foreign debt").

According to the NBU forecasts, payments on the state debt (both repayment of obligations and servicing) in 2024, compared to 2023, will grow by 42.5% — up to UAH 1.03 trillion in total.

Meanwhile, on September 27, 2023, the Government approved the strategy of public debt management for 2024-2026. The document says that wartime brought rapid accumulation of foreign debt, which is used to cover the budget deficit.

Ukraine’s foreign debt at the end of period, $ billion, unless stated otherwise

|

|

2021 |

2022 |

1st half of 2023 |

2023 (forecast) |

|

Total (gross foreign debt) |

129.7 |

131.0 |

148.6 |

160.0 |

|

Public sector |

51.3 |

65.3 |

81.4 |

92.0 |

|

Public sector, % of GDP |

25.7 |

40.8 |

48.0 |

54.0 |

Such accumulation of debts can later be partly offset through restructuring or even written off. However, now, the risks of mounting debt pressure are growing. The NBU and the IMF repeatedly warned and continue to warn about a possible reduction in international aid. Therefore, concessional long-term financing from abroad and increasing the share of grants (to obtain as much funds as possible on concessional terms, to reduce the cost of their maintenance and to extend the terms of debt repayment) are the primary tasks of the government.

In conclusion, we emphasize that despite the enormous hardships caused by Russian aggression, Ukraine has the internal potential to improve socio-economic dynamics, and, as in previous years, we hope that thanks to military successes and partner assistance, institutional changes will accelerate, and this potential will finally begin to work.

https://razumkov.org.ua/statti/vid-poperednikh-pidsumkiv-2023-do-prognozu-2024